July 2022 Bitwise Investor Letter

San Francisco • Jul 12, 2022

In This Issue: On Crypto Cycles, and What Could Stop This Bear Market and Ignite the Next Bull Run

Note: We recently relaunched the Bitwise Investor Letter, our monthly look at the biggest themes shaping the crypto market plus the latest updates on Bitwise. If you're not receiving this letter directly but would like to subscribe, please click here.

Market Overview

Dear Investors,

We are in the midst of a brutal crypto bear market. Historic, even.

Consider these two facts: June was the worst month in bitcoin’s history (-40%), and Q2 2022 was the worst quarter for crypto in more than a decade (-59%).

The last time we had a quarter this bad, bitcoin was trading for less than $20 and Barack Obama was in his first term as president.

The media has been quick to pick up on this trend and extrapolate it down to zero. Some examples:

Bloomberg: A $2 Trillion Free-Fall Rattles Crypto to the Core

The Wall Street Journal: The Crypto Party Is Over

The New York Times: Crashing Crypto: Is This Time Different?

While the details of each article differ, their core message is the same: Crypto is done. Over. Kaput.

Sure, they say, crypto has had pullbacks before. But this time it’s different.

It’s easy to understand the appeal of this message. Bear markets are hard, and this is arguably the most vicious bear market in crypto’s history.

But as crypto skeptics reminded investors on the way up, the four most expensive words in the English language are “this time is different.” And while the intensity of the decline is remarkable, if you zoom out just a bit, the contours look shockingly familiar.

Consider the table below, which shows the annual returns of bitcoin since it started trading in 2011.

The four-year cyclicality of crypto jumps off the page. If you’re wondering why you didn’t sell at the end of 2021, you’re not alone: Hindsight is 20/20.

But rueing the past as you consider this pattern will not help. Instead, you should look to the future. Because the drivers of crypto’s cyclicality show you where to look if you want to find the next potential big bull market.

That’s the topic of this month’s Investor Letter.

What Causes Crypto’s Cycles

The most common explanation for crypto’s cyclicality is that it is driven by bitcoin’s halving cycle. Every four years, like clockwork, the amount of new bitcoin being produced falls in half. This makes bitcoin more scarce, which, the theory goes, makes the price go up.

I wish this were true.

If the bitcoin halving actually drove prices, and you could count on the four-year return pattern to persist, investing would be easy. Just wait until the end of this year, pile in, and then wait for three years before you sell. Rinse and repeat; eventually you’ll be a billionaire.

Alas, it’s not that easy.

Even if it does have an impact, the halving theory can’t explain the entirety of crypto cycles for multiple reasons:

It’s only bitcoin. Why would the bitcoin halving influence the price of other crypto assets?

Halvings don’t sync with big price moves. For instance, bitcoin halved in 2016, but crypto spiked one year later, in 2017. When bitcoin halved again in 2020, prices moved sharply upward. Why are the halvings sometimes aligned with price moves and sometimes not?

It’s not big enough to explain the full cycle. For all we talk about it, halvings are not that big a deal. The 2016 halving, for instance, occurred when bitcoin was trading at $663. At the time, the annualized issuance of bitcoin fell from $436 million to $218 million (based on prices at the time). Over the next 18 months, bitcoin’s market cap rose from $11 billion to $342 billion. Can a $218 million annual reduction in supply really translate to a $331 billion increase in market cap? That’s quite a multiplier.

It should be priced in. The timing of bitcoin halvings has been known (plus or minus a few days) since bitcoin was created. Assuming the crypto markets are even vaguely efficient, the impact should be priced in.

In addition, as a general rule, explanatory models that effectively guarantee future returns are always wrong. While halvings matter to some degree, they can’t and don’t explain the vast majority of crypto’s historical returns.

So what does?

A Radical Theory: Crypto’s Price Rises When It Creates Products People Want

I have a much simpler view of what drives crypto’s cyclicality: Prices rise when the industry discovers products people want to use.

It feels ridiculous to write that sentence because, well, duh—but for some reason, it’s never discussed.

And yet, viewed through this lens, crypto’s returns make all the sense in the world.

In 2011 and 2013, crypto’s first big up years, the product that people wanted to use was bitcoin itself.

2011 was the first year that bitcoin traded, and 2013 was the first year that the general public could broadly access it; Coinbase, for example, launched in October 2012. Prior to 2013, you had to be a computer scientist or cryptographer to meaningfully participate in the space. 2013 positioned bitcoin as a mainstream investment.

In 2017, the story was different.

Ethereum was created in 2015, offering a more flexible blockchain than bitcoin. Entrepreneurs spent years figuring out what to do with its new capabilities. In 2017, they found a killer app: the initial coin offering (ICO). It turns out you could use the Ethereum blockchain to raise money for new projects, in a manner similar to an initial public offering (IPO).

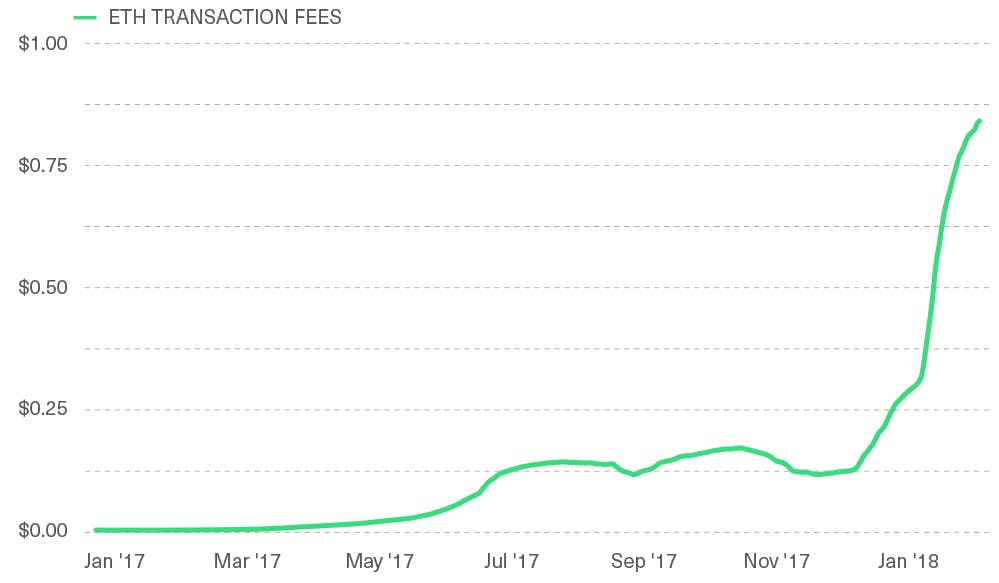

While ICOs operated in a regulatory gray area and were often of dubious quality, they were also highly popular: Investors poured more than $4.5 billion into ICOs in 2017. This sparked huge demand for Ethereum. The best way to visualize this demand is to consider the median fee a person paid to process a transaction on Ethereum. This toll—called a “gas fee”—rose from less than $0.01 at the end of 2016 to roughly $0.33 one year later, en route to nearly $2.92 by mid-January 2018.

Ethereum Gas Fees, Which Reflect Blockchain Usage, Trended Up During the ICO Cycle

Ethereum transaction fees* between January 2017 and January 2018 (USD)

Source: Bitwise Asset Management with data from Coin Metrics.

* Note: Fees depicted as a 60-day simple moving average.

The 2020 boom—which actually stretched from March 2020 to November 2021, a period when bitcoin rose from roughly $5,000 to more than $68,000—was driven by multiple products landing at once.

Stablecoins, decentralized finance (DeFi), and non-fungible tokens (NFTs) all came into bloom during this period. Consider that from March 1, 2020 through November 30, 2021:

Stablecoin total market cap rose from $7.5 billion to more than $147 billion, an almost 20-fold increase;

DeFi’s total value locked jumped from roughly $842 million to $246 billion, a nearly 300-fold increase; and

Monthly NFT trading volume increased from effectively $0 to more than $2 billion.

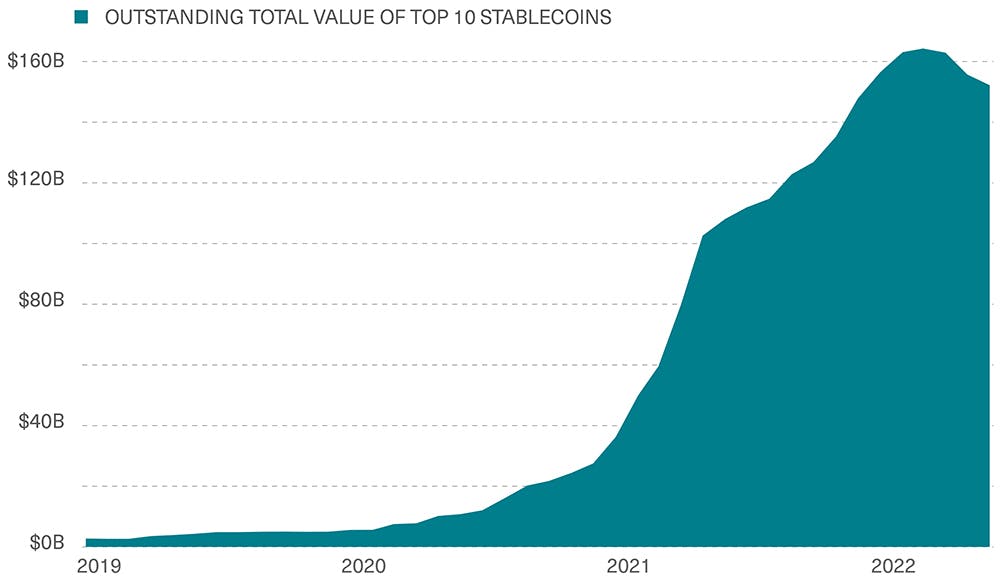

Stablecoins Rose to Prominence in 2020 and 2021

Combined market cap of top 10 stablecoins* between January 2019 and June 2022 (USD billions)

Source: Bitwise Asset Management with data from Statista.

* Note: Top 10 stablecoins include: Binance USD (BUSD), Pax Dollar (USDP), Fei USD (FEI), Tether (USDT), Dai (DAI), Neutrino USD (USDN), Gemini Dollar (GUSD), USD Coin (USDC), TrueUSD (TUSD), USDD (USDD).

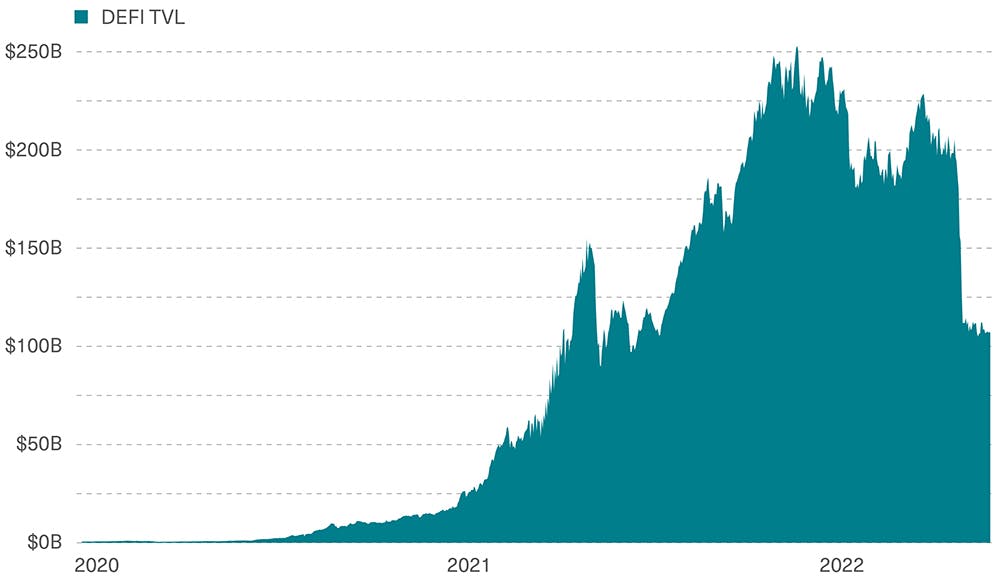

Post-Correction, Total Capital Allocated in DeFi Is Still Over $100 Billion

Total Value Locked in DeFi protocols between January 2020 and June 2022 (USD billions)

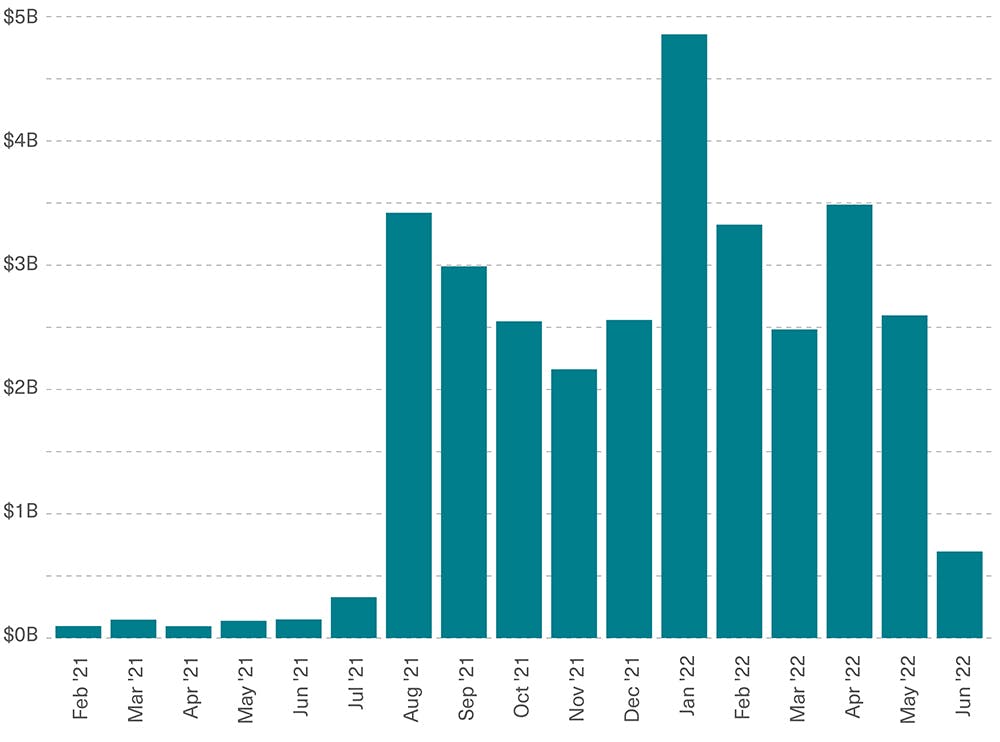

NFTs Stormed Into the Mainstream in August 2021

Monthly NFT Trading Volume on OpenSea* between February 2021 and June 2022 (USD billions)

Source: Bitwise Asset Management with data from Dune Analytics.

* Note: Data includes only Ethereum-based NFTs.

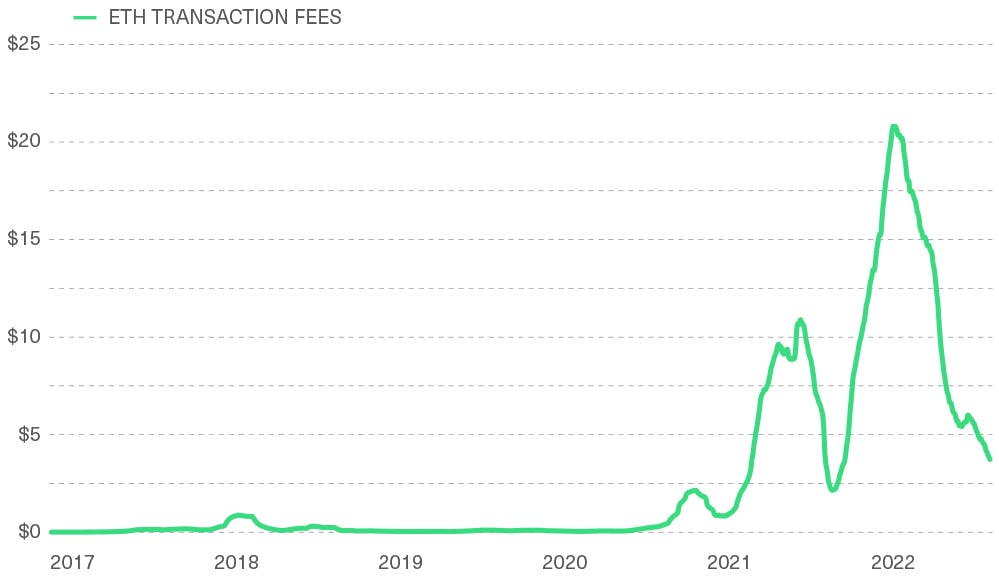

Once again, we saw this trickle through to blockchain activity: The median fee to process a transaction on Ethereum spiked to more than $33 by November 2021, more than 8,000 times December 2016 levels.

Ethereum Fees Continued To Rise With More Blockchain Activity in 2020 and 2021

Ethereum transaction fees* between January 2017 and June 2022 (USD)

Source: Bitwise Asset Management with data from Coin Metrics.

* Note: Fees depicted as a 60-day simple moving average.

Unfortunately, just as quickly as these booms arose, they receded. In each case, we can point to a singular event that ended the bull run:

In 2014, the first application for approval to launch a spot bitcoin ETF in the U.S. was delayed indefinitely following negative feedback from the SEC. This dashed hopes that it would quickly become a mainstream asset, and prices collapsed.

In 2018, regulators cracked down and essentially ended the ICO market, sending crypto into a deep freeze.

In November 2021, the Federal Reserve switched from quantitative easing to quantitative tightening, sucking the wind out of the speculative fervor that had driven interest in NFTs and DeFi. Companies that had stretched their balance sheets too far found themselves in dire straits.

Critics will look at this list and ask, why bother? If the tide goes out as quickly as it comes in, investing is simply a game of chance, unmoored to actual value creation.

The answer, of course, is that historically each wave is bigger than the last.

Yes, crypto pulled back in 2014 … but bitcoin didn’t go away.

Yes, the ICO crackdown sent us into a crypto winter … but the ICOs acted as a proof of concept for the DeFi boom in 2020.

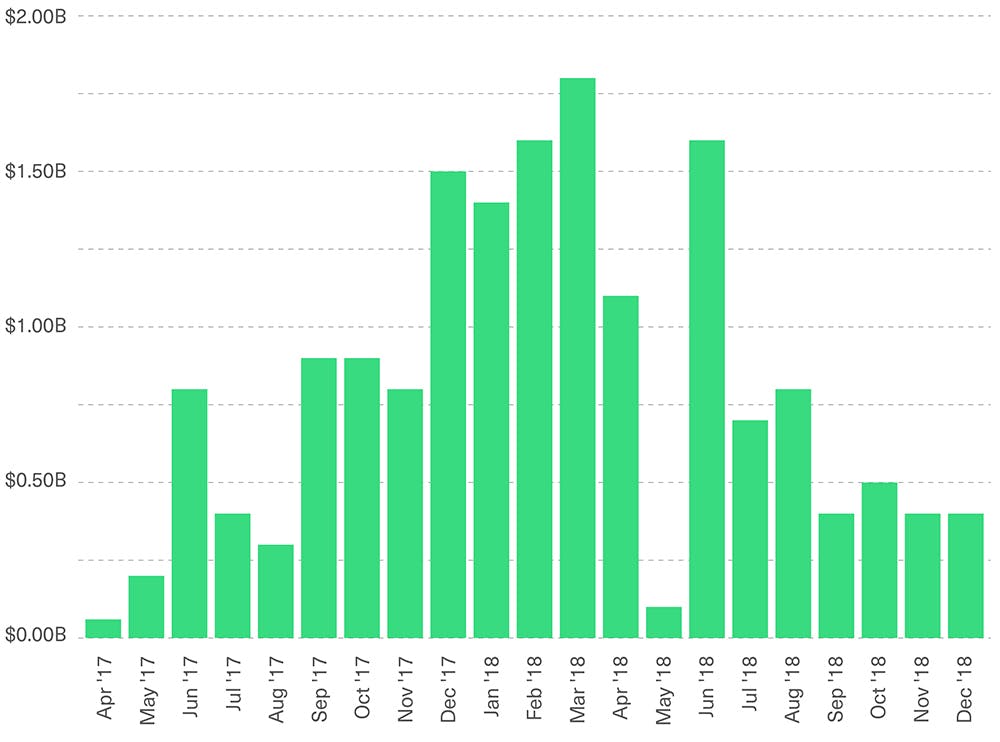

ICOs Vanished in 2018 … but Led the Way to the DeFi Boom Two Years Later

Amount of funds raised for cryptocurrency initial coin offering (ICO) projects worldwide between April 2017 and December 2018 (USD billions)

Source: Bitwise Asset Management with data from Statista.

And yes, the risk-off environment has taken the starch out of the NFT and DeFi markets, but both are still significant. As are stablecoins. Moreover, the surrounding boom brought to the space billions in venture capital that should open the door to more building.

It’s frustrating that the market is so volatile; the boom-and-bust cycle is emotionally exhausting and bad for investors. But we believe the long-term pattern still points upward.

Where Do We Go From Here?

All of which brings us to today.

In the short term, crypto’s fate rests on the outlook for the macro environment and the ongoing crypto deleveraging process. Worsening macro conditions or additional credit failures could lead to another leg down in prices.

But our simple mental model—that crypto’s cycle is driven by delivering products that people want to use—paints a much brighter picture.

Looking out, not over two months but over two years, the preconditions for the next potential bull market are easy to spot.

You still have the core capabilities of crypto and blockchains: moving money and financial goods at the speed of the internet; allowing developers to program money like software; and creating digital property rights. On top of that, you have the $33 billion in venture capital that flowed into the crypto ecosystem in 2021; record numbers of developers operating in the crypto market; and an improving regulatory environment.

In addition, the core technology behind the boom—blockchain itself—is improving quickly.

One of the things that halted the 2020-2021 boom, even before the Fed raised rates, was that leading blockchains like Ethereum simply got too crowded, like the internet in the pre-broadband era. At the peak of the bull market, things were so congested that it cost more than $50 to do a single transaction on Ethereum. Think about all the applications this renders impossible; imagine if it cost $50 every time you used your credit card.

But within the next few years, Ethereum’s throughput is expected to increase 1,000-fold or more. And already, alternative blockchains like Solana and scalability solutions like Polygon are lowering fees and improving bandwidth. This creates a playground for entrepreneurs to build the next big thing.

What could that be? It’s hard to say, but these are some areas I’m keeping an eye on:

Stablecoins: Among other uses, stablecoins provide access to dollars for challenged or emerging economies. With inflation running rampant in many areas of the world, one can imagine stablecoins swelling to $1 trillion or more in the coming years.

DAOs: Decentralized autonomous organizations (DAOs) never really went mainstream in 2020 or 2021, but they offer a revolutionary way to organize groups of people behind economic activities. DAOs today remind me of NFTs in 2017 … present, but waiting for their moment to shine.

Institutional DeFi: DeFi apps like Uniswap and Aave have proven themselves over the past few years, but mostly for retail customers. Regulatory advances could open that up to much larger institutional markets. Already, entities like MakerDAO are striking deals with local banks to manage hundreds of millions of dollars in debt.

Regulated crypto: Things are heating up in Washington, with progress on stablecoin regulation and rising hopes for comprehensive crypto regulation, including the possibility of bringing crypto exchanges inside the purview of the SEC. While that could be an awkward transition, it would have massively positive downstream effects. Among other things, it would make spot ETFs a layup and allow crypto entrepreneurs to build a meaningful alternative to Wall Street.

Web3: Web3 is an umbrella term that captures a movement to build a new version of the internet. This evolved internet would be built on blockchain and would allow users to own their own data (as opposed to companies owning user data, as they do today). Web3 startups have attracted billions in venture capital activity in the past year.

Digital identity: One of the biggest new ideas coursing through crypto is the concept of digital identity: using cryptographic technologies to create passports and verify identity on the internet. While still early, digital identity solutions could recode how much of the online economy works.

Crypto gaming: Crypto gaming has grown in fits and starts over the past few years, with occasional booms (CryptoKitties, Axie Infinity) followed by periods of relative quiet. But engagement on crypto games has never actually gone away: Monthly active-user metrics of such games have held steady over the past year. Could a breakthrough boom be around the corner?

NFTs (beyond art): NFTs burst onto the scene in 2020, mostly as ownership devices for digital pictures. But NFTs can be used for much more than art: They can be applied to music streaming rights, medical records, and more. NFTs may be the most powerful technological capability that crypto-enabled blockchains create, and we’re just scratching the surface of their uses.

Payments: The aforementioned improvements in the throughput of public blockchains could finally allow crypto to provide a meaningful payments platform for real-world assets. Previous attempts have been hampered by crypto’s limited capabilities and occasional high fees, but those may soon be a thing of the past.

If this looks like a laundry list, that’s because it is. There is so much bubbling beneath the surface of the crypto bear market that it’s hard not to be excited about what’s next. (And that’s not even accounting for the ideas that I’m not thinking of yet!) Reviewing the list, it’s easy to see a coming boom in crypto usage potentially 10 times bigger than the last.

Every major bull market in crypto’s history has been started by a breakthrough product. This one is likely to be the same.

Matt Hougan

Chief Investment Officer

Notes From the Research Desk

Our research team captures some of crypto’s biggest themes and highlights in a word (or so).

What does a recession mean for crypto?

Once the shockwaves of the current crypto credit crisis settle down, I suspect the next question on investors’ minds will be, how does crypto fare in a recessionary environment?

While the jury is still out on whether a recession will come to the U.S., over the last month market consensus seems to be slowly moving in this direction. Economists from Bloomberg and Goldman Sachs, for instance, recently put the chances of a recession over the next 12 months at 38% and 30%, respectively, up from essentially zero a few months ago. And the spread between 2- and 10-year Treasury bonds just turned negative—historically a harbinger of a downturn.

If this scenario materializes, I think an interesting question will be whether economic downturns, which tend to directly affect many companies' revenues and earnings, will also affect crypto. In normal times, crypto tends to respond most to fundamental drivers other than earnings, such as technological development, regulatory developments, and broader public adoption.

David Lawant

Director of Research

A faster competitor snatches business from Ethereum

One of crypto’s biggest decentralized exchanges, dYdX, recently announced it’s leaving Ethereum to launch its own blockchain on the Cosmos network. Think of Cosmos as a sort of European Union of blockchains—it’s a central entity on which different blockchains can be built, allowing them to be interconnected beneficiaries of the platform, but still distinct.

This is big news. It reinforces a continued problem of Ethereum’s—high fees and congestion—which is causing users like dYdX to look for more innovative alternatives. But, of course, there are tradeoffs: While Cosmos will likely help dYdX process large-scale transactions much more quickly, it’s not as secure as Ethereum. In the long run, Cosmos is likely to enhance its security just as Ethereum will improve on scalability. But the latest move from dYdX may signify a longer-term trend of faster competitors siphoning business from Ethereum.

DeFi lenders: From outlaws to outliers

Amid a sweeping credit crisis, blue-chip DeFi lenders have emerged as crypto’s dark horse. While centralized crypto lenders like Celsius faced insolvency in recent weeks, decentralized lending protocols like Aave, Compound, and Maker proved resilient. And as crypto hedge funds like Three Arrows Capital were collapsing and ghosting creditors, DeFi lenders were autonomously processing margin calls and liquidations as designed. In fact, June’s $160 million in DeFi liquidations was in line with the monthly average—all at a time when centralized-finance competitors were imploding. And while it’s true that DeFi assets have suffered alongside other crypto assets, there’s a bigger story: The resilience of leading DeFi lenders in extreme markets has shown the strength of their risk management systems.

Ryan Rasmussen

Head of Research

Storm clouds for miners … and silver linings

It’s been a tough month for crypto miners. The combination of rising energy costs, falling crypto prices, and hefty liabilities incurred during the bull run have put new pressure on the companies responsible for validating blockchain transactions and securing crypto networks.

Some recent examples: Marathon Digital Holdings (MARA) saw more than 75% of its mining operations halted after a major storm took out a power station in Montana, highlighting the critical importance of sound risk management strategies. (The company expects some of the 30,000 rigs to come back online in early July.) And in June, publicly traded miners sold more bitcoin than they produced, a contributing factor to bitcoin’s 57% year-to-date decline.

There are a few silver linings, however: 1) As of Q1 2022, the cost of mining bitcoin for public miners ranged from roughly $6,000 to $18,000, which means most miners are still profitable or near breakeven at today’s prices; and 2) Many miners accumulated significant cash and bitcoin reserves during the run-up, giving them the clout to not only weather a downturn but continue building. For a deeper dive into miners’ fundamentals, check out our research team’s recent piece here.

Juan Leon, CFA

Senior Investment Strategist

Alyssa Choo

Crypto Research Analyst

Performance

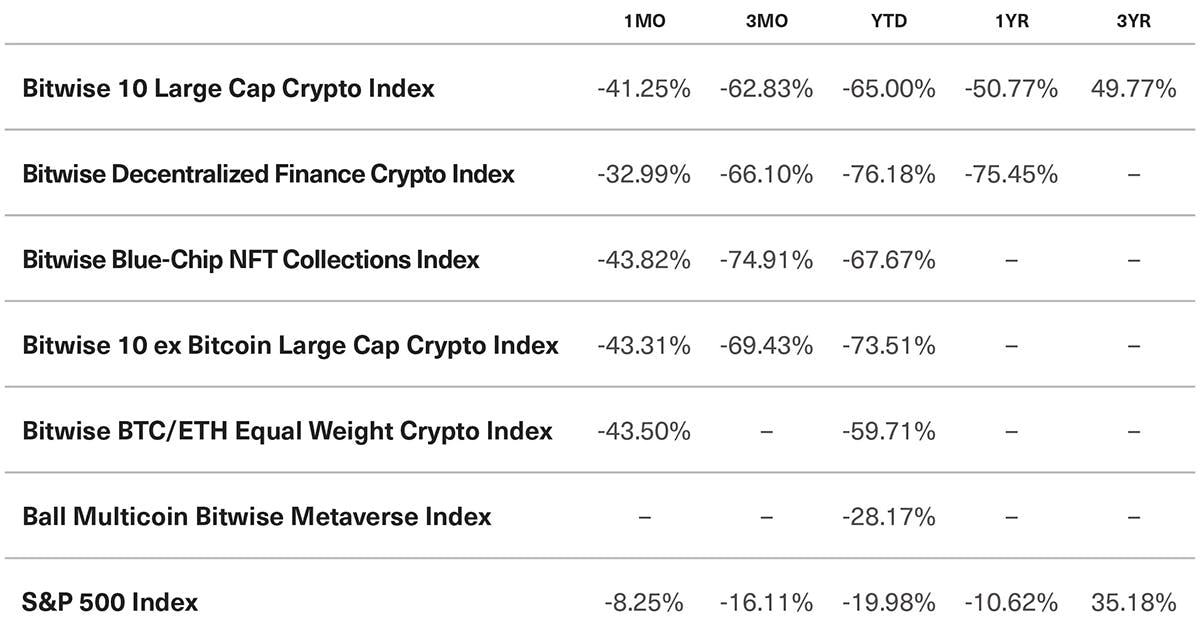

The recent credit events discussed above left a mark on crypto’s returns in June. The Bitwise 10 Large Cap Crypto Index was down 41% during the month—led by Ethereum’s and bitcoin’s 47% and 40% respective declines—bringing the overall index down 65% year-to-date. A similar trend played out in other areas of crypto: In June, the Bitwise Blue-Chip NFT Collections Index was down 44%, and the Bitwise Decentralized Finance Index fell 33%.

Benchmark Performance as of June 30, 2022

* Indexes that incepted after January 1, 2022 display performance since inception in the YTD column. The Bitwise BTC/ETH Equal Weight Crypto Index incepted on April 18, 2022, and the Ball Multicoin Bitwise Metaverse Index incepted on June 6, 2022.

Source: Bitwise Asset Management with data from IEXCloud.

Notes: It is not possible to invest directly in an index. Past performance is no guarantee of future results. The Bitwise 10 Large Cap Crypto Index captures the 10 largest eligible crypto assets by free-float-adjusted market capitalization. The Bitwise Decentralized Finance Crypto Index is designed to provide investors with a clear, rules-based, and transparent way to track the value of the rapidly emerging Decentralized Finance space. The Bitwise Blue-Chip NFT Collections Index is designed to broadly capture the investable market opportunity for the most valuable arts and collectibles NFT collections. The Bitwise 10 ex Bitcoin Large Cap Crypto Index captures the assets in the Bitwise 10 Large Cap Crypto Index, excluding bitcoin. The Bitwise BTC/ETH Equal Weight Crypto Index captures the value of an equal-weighted index consisting of bitcoin and ethereum. The Ball Multicoin Bitwise Metaverse Index is designed to capture the investable market opportunity for crypto assets exposed to the emerging Metaverse. The S&P 500 Index, or Standard & Poor's 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

What's New at Bitwise?

Noteworthy happenings and key milestones.

The SEC Denied Our Spot Bitcoin ETF; We Responded

On June 29, the SEC rejected applications from Bitwise and Grayscale for spot bitcoin ETFs. It was a disappointing result, particularly considering the potential for ETFs to reduce costs, increase transparency, and raise investor protections.

READ MOREStablecoins: Separating the Wheat From the Chaff

Stablecoins have exploded in popularity in recent years. But as the recent Terra/Luna implosion showed, they’re not all created equal. In this brief, research team members Ryan Rasmussen and Gayatri Choudhury explain what stablecoins are, how they differ from one another, and why U.S. regulators should embrace them.

READ MOREFive Takeaways from Consensus 2022

In June, 17,000 people gathered in Austin for Consensus, the largest crypto conference in the country. Couldn’t make it? Fear not: Three members of Bitwise’s research team recently summed up the top five takeaways. (The third explains why Amazon should be nervous.)

READ MOREWhy Bitcoin Miners Deserve a Closer Look

What do bitcoin miners do? How are their businesses faring in the downturn? And why could some of them be well positioned to lead a bitcoin recovery? Our research team has answers.

READ MOREMore Quick-Hit Educational Videos

Our latest batch of 30-second videos on CNBC featured Bitwise CEO Hunter Horsley discussing a staggering statistic on crypto wallets, the reason there are 10,000 crypto assets, and why crypto indexes can be so powerful.

Select Media Appearances

CNBC’s Crypto World: Potential catalysts for a market rebound—and which altcoins show promise

Wealthtrack with Consuelo Mack: The compelling case for crypto (even now)

U.S. News & World Report: Katherine Dowling on the biggest problem in current regulatory discussions

Fortune: Is this the time to buy? Or are there more shoes to drop?

Upcoming Conferences

Going to any of these upcoming events? So is Bitwise. We’d love to connect in person. Email advisors@bitwiseinvestments.com if you’d like to set up a one-on-one meeting.

DACFP Bitcoin Mining Virtual Conference | July 20

Titan RIA Retreat | July 20-21 in Newport, RI

Wolfgang Advisor Conference | July 21 in Wayne, NJ

Bitwise Asset Management is a global crypto asset manager with $9 billion in client assets and a suite of over 70 investment products spanning ETFs, separately managed accounts, private funds, hedge fund strategies, and staking. The firm has a nine-year track record and today serves more than 5,500 private wealth teams, RIAs, family offices and institutional investors as well as 21 banks and broker-dealers. The Bitwise team of technology and investment professionals is backed by leading institutional investors and has offices in San Francisco, New York, and London.