Staking as a Service: An Emerging Crypto Sector Poised for Growth

San Francisco • Sep 16, 2022

This week, Ethereum completed a technical upgrade called "The Merge" that changed the network's "consensus mechanism" from Proof-of-Work to Proof-of-Stake. The change is expected to cut Ethereum's carbon consumption by 99%, reduce its inflation rate by 75%-90%, and introduce the potential for long-term investors to earn a 4-8% yield on their position through staking.

This change is reshaping the crypto economy, pushing the idea of staking front and center in investors' minds. Among other impacts, it has given rise to a new generation of service providers who help investors stake their assets and earn that yield. This column focuses on the rise of these Staking as a Service providers, analyzing how they work, the available yields, their trade-offs, fees, and relative market shares.

Why Do People Stake Crypto Assets?

Staking involves making a financial commitment to a blockchain in its native asset to secure the network. It's a fundamental component of blockchain infrastructure because of the security and decentralization it provides.

The incentive for users to stake crypto assets is to earn additional yield. The yield comes from transaction fees paid by users of the network and new issuance of the network's native crypto asset. Different blockchains offer different yields (Ethereum is not the only blockchain that allows staking), and those yields vary over time based on multiple factors, including how many holders participate in the staking process, the pro rata share of the total staked supply, and other variables related to network use.

For Ethereum, the combined APY for those participating in staking could reach up to 8%. While those yields could fall in the long run as more participants enter the market and saturate the distribution of staking rewards, it's projected to remain in the 4-8% range.

However, staking isn’t without its risks and challenges. One challenge is that, until recently, staking was hard for most investors to access due to high capital commitments and sophisticated hardware requirements. For example, staking on Ethereum requires operating and maintaining a dedicated computer connected to the internet 24/7/365 (known as a "validator") and depositing a minimum of 32 ETH to activate the validator software (that's ~$50,000 at the current prices).

Another risk associated with staking is the potential for one's staked assets to be forfeited or "slashed." This design mechanism helps to ensure that validators consistently enforce network security. Suppose someone running their Ethereum staking infrastructure misses a software update or has a power outage; in that case, even though there is no malicious behavior being conducted, the network's security is negatively impacted, so a portion of that user’s staked ETH is automatically slashed. In some ways, slashing is similar to the fees that banks take from customer accounts when they don't meet the minimum balance and other requirements.

Staking on Ethereum highlights another downside to the process: Staked assets are often subject to a lock-up period that, in some cases, can be relatively long. For example, ETH staked on Ethereum's Beacon Chain—a pre-launch test network for The Merge, which began in December 2020—will be locked until March 2023 (at the earliest). That creates significant risk given Ethereum's price volatility; a 4-8% yield is cold comfort if the market falls significantly. Nevertheless, locking staked ETH is necessary to enforce slashing, and the staking rewards reflect this risk: Ethereum's earliest stakers received an APY of over 20%.

These obstacles have led to a new category of service providers that lower the financial and technological barriers associated with staking by pooling and staking crypto assets on behalf of customers. Staking as a Service ("STaaS") providers handle the technical challenges, costs, and risks associated with the different aspects of staking, offering an alternative to investors who want access to staking yields but don't have the technological know-how, capital requirements, or risk appetite to stake assets on their own.

Beyond handling the technical nuances of staking, one significant value proposition of StaaS is that if something goes wrong with the providers' validators, they generally take the hit for slashed assets, not the customer.

How Have Staking as a Service (STaaS) Providers Grown?

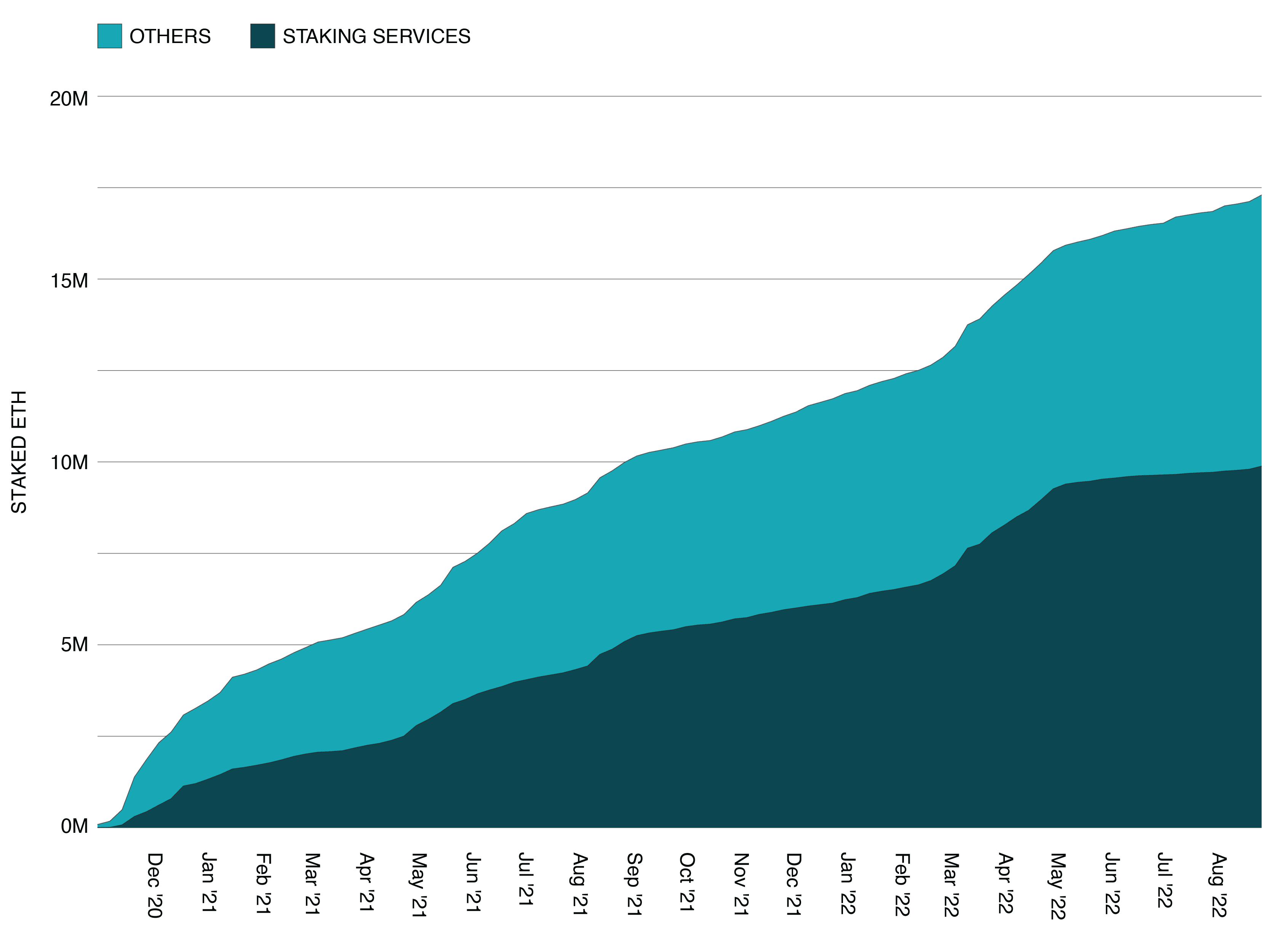

So far, STaaS providers are carving out a significant portion of the staking market. Leading up to The Merge, they represented over 50% of the $21.1 billion ETH staked on Ethereum.

Staking Service Providers Represent More Than 50% of Total Value Staked on Ethereum

Staked ETH on Ethereum using staking services versus other methods from November 2020 to August 2022

STaaS providers earn a portion of the staking yields generated by customers' staked assets in exchange for their services. And it's no pocket change: Lido, the leading DeFi staking application, generated more than $300 million in revenue over the past year (pre-Merge!).

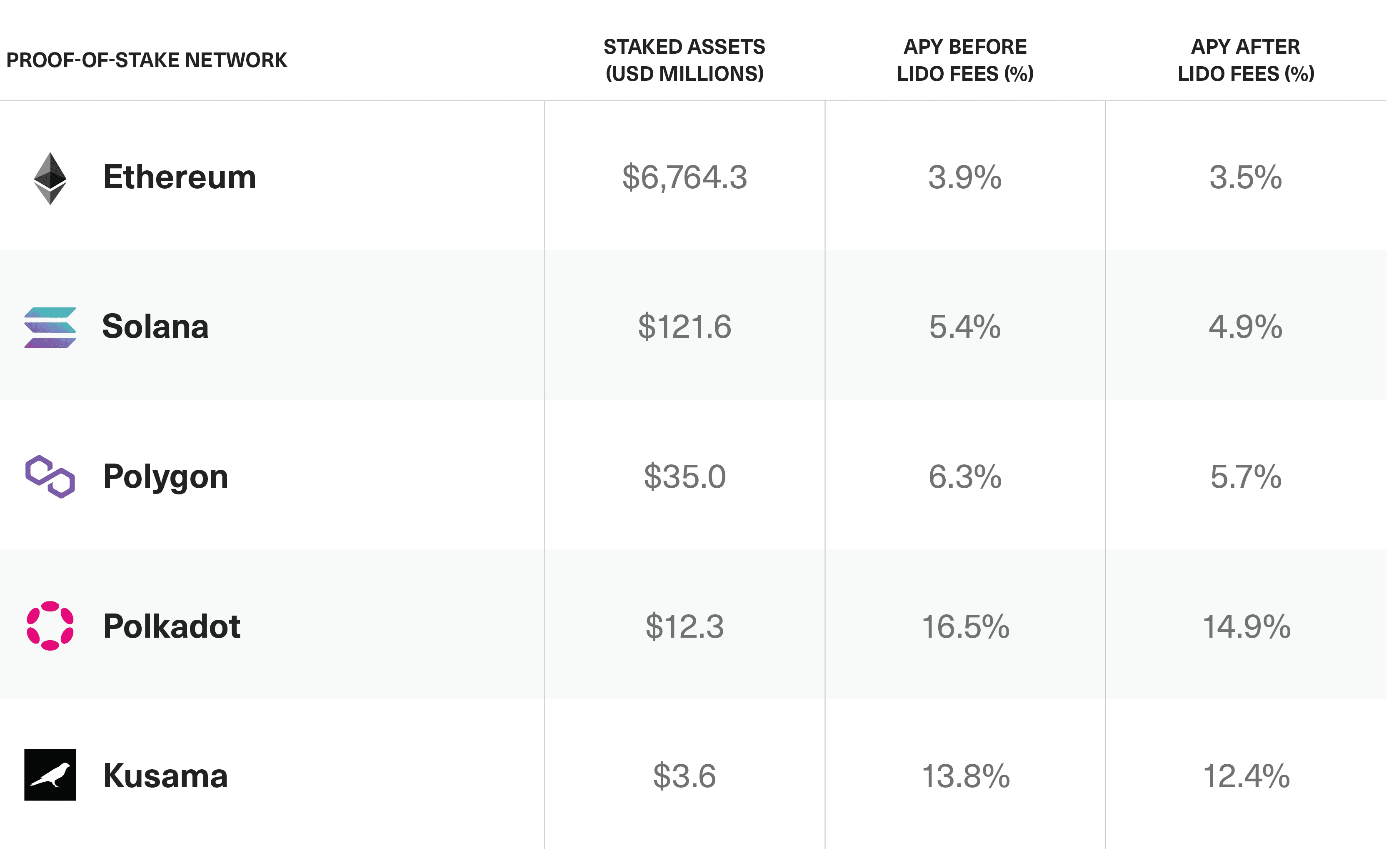

Most staking services are blockchain-agnostic, meaning they support multiple Proof-of-Stake (PoS) blockchains. Lido, for example, supports Ethereum, Solana, Kusama, Polygon, and Polkadot, each of which has different nuances to staking and provides a different APY. The table below shows the APYs for staking with Lido across the various PoS chains they currently support.

Lido APY and Fees for Staking on Different Proof-of-Stake Networks

Comparing Staking as a Service Providers

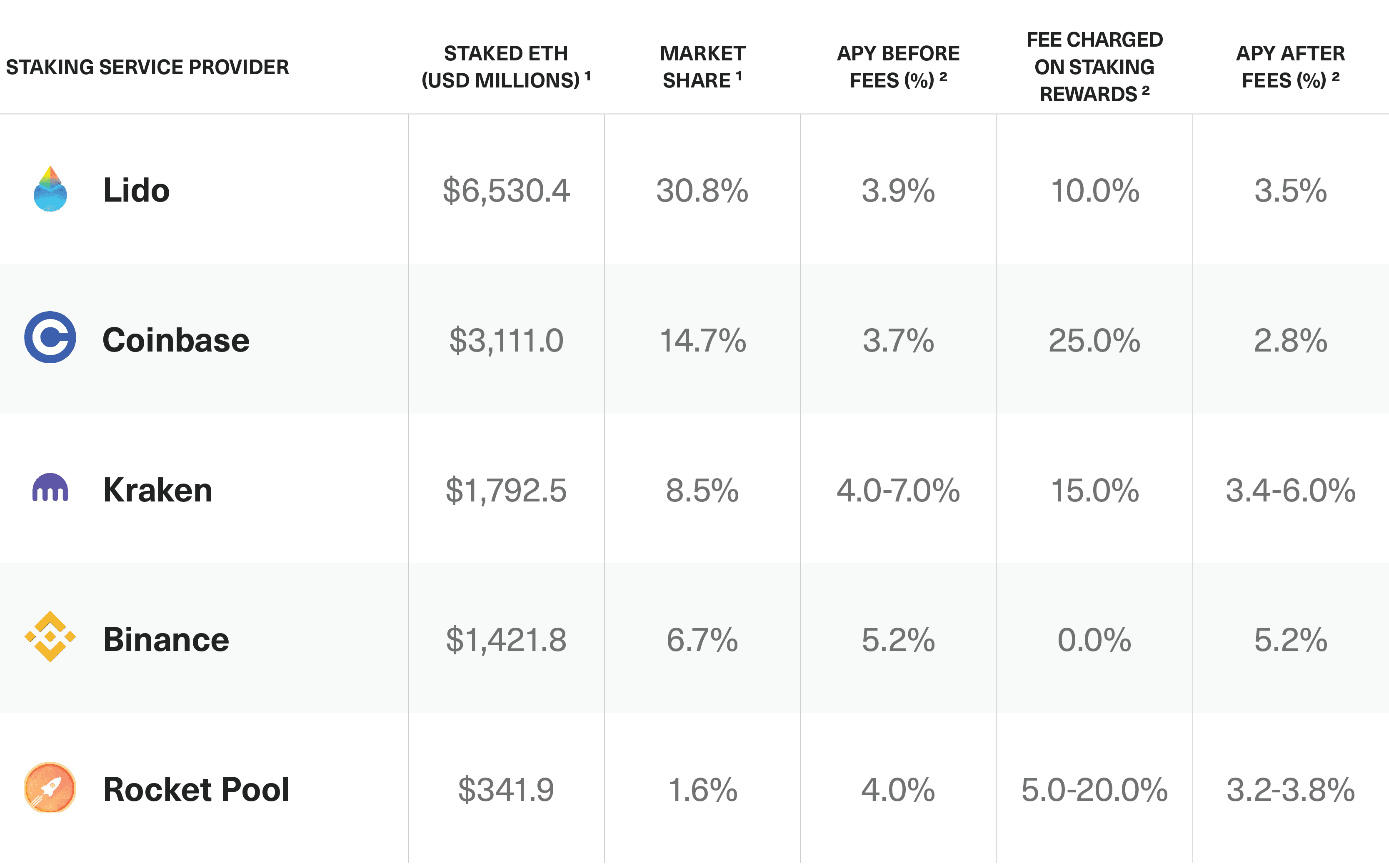

STaaS providers take several forms, from DeFi applications, like Lido and RocketPool, to companies that trade on the NASDAQ, like Coinbase. The table below provides an overview of the leading Ethereum staking service providers, including their current APY on staked ETH, the fees they charge, and their relative market share.

The Leading Staking Service Providers Represent $13.2 Billion of Staked ETH

Overview of the leading staking service providers for Ethereum as of August 31, 2022

Centralized vs. Decentralized Services

The biggest competitive battle in the Staking as a Service space is between centralized and decentralized services, which offer different core value propositions to customers.

Centralized exchanges like Kraken and Coinbase have succeeded in the staking business by taking advantage of their positioning in the crypto market. Users have grown fond of the one- or two-click features offered in their mobile applications, and institutions prefer centralized exchanges because they are U.S.-based and operate within the U.S. regulatory framework.

However, staking with centralized service providers can have its drawbacks. For example, for networks with a lock-up period on staked assets, staking with centralized exchanges can be a one-way transaction until the assets are unlocked. In addition, a layer of trust is required between users and centralized services, as most centralized STaaS solutions are custodial.

DeFi alternatives that offer more liquidity and require less trust have emerged. These services, also called “liquid staking,” have two significant differences from their illiquid counterparts. First, once an investor stakes their assets, the service provider issues the investor a separate token that represents the investor's claim on their staked assets plus the accrued rewards. This token, known as a "liquid staking derivative" or "LSD," can be used as collateral for borrowing against or earning yield on DeFi applications like Aave and Curve. Second, if a user needs to sell their position before their staked assets are unlocked, they can sell this LSD on the secondary market. In this way, the LSD allows users to escape the liquidity constraint of locking up assets. It's not a risk-free transaction, however: During times of volatility, LSDs can trade at discounts to fair value, reflecting the "cost" of this liquidity.

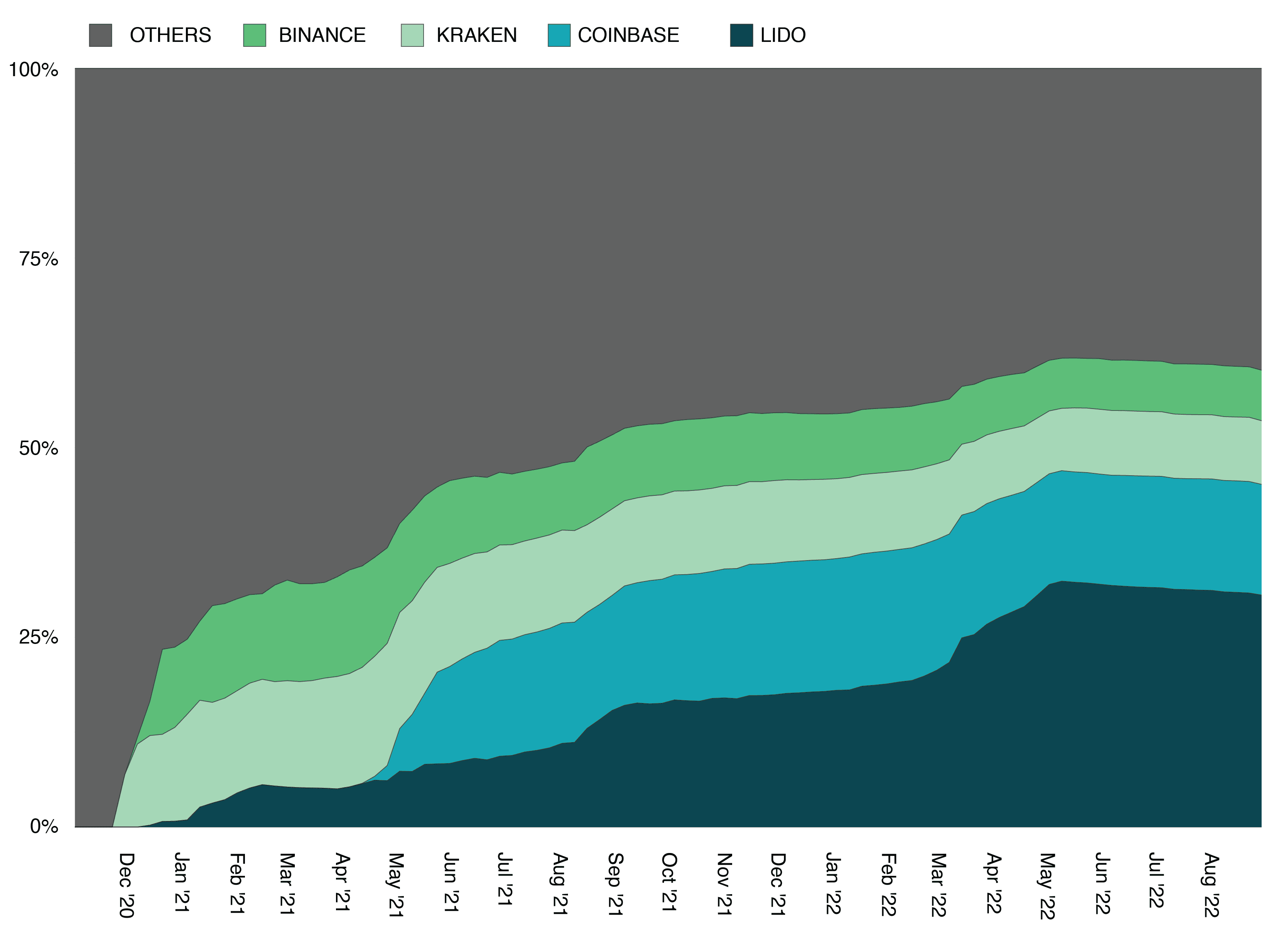

Bringing interoperability and liquidity to staked assets is valuable to users and investors, as evidenced by the sheer demand for liquid staking solutions: Lido has more than $7.4 billion in staked assets across the five blockchains it supports and enjoys a 30.1% market share of total staked ETH. Perhaps that’s why Coinbase is launching a new liquid staking product for staked ETH called cbETH.

Lido Enjoys a 30.1% Market Share of Total Value Staked on Ethereum

Relative share of total value staked on Ethereum by entity from November 2020 to August 2022

Lido's stETH token is the most popular liquid staking derivative. Currently, there is $2.3 billion in stETH deposited as collateral in DeFi lending apps like Aave and Maker. Meanwhile, one of the leading decentralized exchanges, Curve, has $1.1 billion of liquidity for the stETH trading pairs. So not only are investors diving head first into staking, but they are leveraging liquid staking services and the composability of DeFi to amplify the APY and utility of assets they are already staking.

The Opportunity Size in Staking as a Service

Staking as a Service has already gained remarkable traction. The fact that the dominance of proof-of-stake networks relative to the entire crypto market is snowballing is a promising indicator that the demand for STaaS will continue to grow.

The overall shift of the crypto market from PoW to PoS is one reason why JPMorgan estimates that staking will gain traction as a source of revenue for institutional and retail investors and that staking could grow to an industry generating more than $40 billion in revenue annually.

We expect the STaaS market to become more competitive as new providers rush in to take advantage of the opportunity staking represents. That will be good for crypto generally, increasing the network's resiliency and diversifying risk among more participants—that is the point of staking, after all. While it's unclear who the long-term market leader in the space will be—whether centralized or decentralized staking providers, or a new type of STaaS provider we've yet to see—one thing appears to be very likely: As PoS blockchains grow, Staking as a Service providers are well-positioned to benefit from that growth.

Bitwise Asset Management is a global crypto asset manager with $9 billion in client assets and a suite of over 70 investment products spanning ETFs, separately managed accounts, private funds, hedge fund strategies, and staking. The firm has a nine-year track record and today serves more than 5,500 private wealth teams, RIAs, family offices and institutional investors as well as 21 banks and broker-dealers. The Bitwise team of technology and investment professionals is backed by leading institutional investors and has offices in San Francisco, New York, and London.