Timely Insights

Forged in the Fire: The Emergence of Dynamic Risk Management as a Key Advantage for DeFi

San Francisco • May 9, 2022

In the recent media narrative around Decentralized Finance (DeFi), one word you are not likely to hear is “robust.”

So it may come as a surprise, for those who haven’t been closely following the DeFi story, to learn just how smooth, resilient, and—yes—robust the operations of DeFi credit markets have become. Not just through periods of unparalleled growth, but also through significant price swings in the crypto market.

The improved risk management practices of DeFi protocols, and the improved capital efficiency in DeFi credit markets that has resulted, have become among the most important—and also most overlooked—aspects of the growing DeFi space. The effective operations of the leading lending protocols under volatile market conditions show how dynamic risk management has become a top priority, and key driver of growth, as they continue to scale up operations.

This is a story of stability forged in the fire of volatility. Understanding how DeFi achieved its hard-won stability can teach us a lot about how innovation in DeFi is driving towards more system-wide resilience, positioning DeFi to compete with—and improve on—the legacy financial system.

A Brief History of DeFi Lending

While DeFi credit markets currently represent the second-largest sector in DeFi, with a combined market cap of $8.5 billion and more than $50 billion in total deposits, they have not always operated smoothly. For example, at the onset of the COVID crisis in March 2020, when prices of major crypto assets crashed by more than 50% and volumes on decentralized protocols spiked, the liquidation process that most DeFi lending protocols rely on temporarily failed, leading to millions of dollars in liquidations which, in theory, could have been avoided.¹

These events left their mark on the industry. Still, the leading players persevered and implemented lessons learned, becoming more sophisticated than ever in managing risk and optimizing for growth and resilience. As a result, a categorical transformation is underway in a system that is focused on fine-tuning stability and scalability.

In May 2021, for example, the price of ETH dropped by 41% in a single day, and the two leading lending protocols, Aave and Compound, processed $330 million in liquidations marking the largest single-day liquidation total ever. Yet, despite having more than 100x the total assets as in March 2020, the protocols performed as designed during these extreme conditions.²

Aave and Compound also worked as intended during the market correction of January 2022. Despite drawdowns in collateral ranging from 5% to 30%, there were no meaningful insolvencies during the market crash (the largest insolvency was an account valued at ~$500 that was too small to be worth liquidating). Moreover, during the sharp market downturn in January 2022, Aave and Compound successfully liquidated $205 million in collateral across 2,500 positions and 1,300 users without a glitch.³

At first glance, the growth in liquidations shown in the chart below might seem to imply that the risk in DeFi credit markets is growing. However, a closer look reveals that a shift occurred after the record liquidations in May 2021; since that point deposits have fluctuated without corresponding spikes in liquidations. Behind those numbers, the systems for managing risk and the capital efficiency in DeFi have been improving.

DeFi Credit Protocols Have Been Successfully Processing Liquidations Under a Wide Range of Market Environments

Average monthly deposits (left axis) and total monthly liquidations (right axis) on Compound and Aave between January 2020 and April 2022 (USD billion)

The improved performance of DeFi isn't a coincidence. Instead, it's a result of the dynamic, data-driven approach to risk management Defi protocols are embracing to optimize for growth and resilience.

A Primer in the Risk Management of DeFi Credit Markets

How has DeFi achieved this stability? What is the system that has been forged in the fire of crypto market downturns, and how does it work?

To back up for a moment, most of the activity in DeFi credit markets involves depositing well-established crypto assets like ethereum into "lending pools" and using these assets as collateral to borrow stablecoins. Generally, the use cases include optimizing yields, trading on leverage, or taking advantage of arbitrage opportunities across the sector.

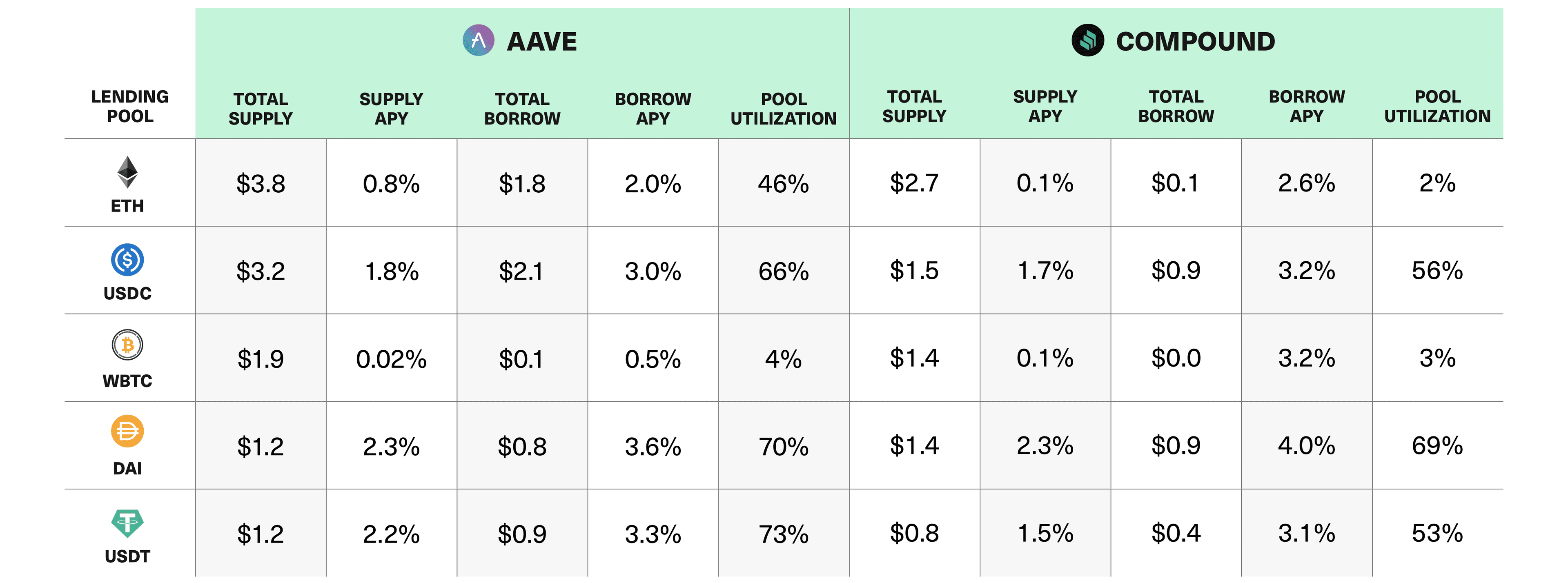

The table below shows the top five pools for Aave and Compound, their respective total supply, total outstanding loans, and annualized interest rates (or "APY") to lend and borrow. The utilization rate indicates the percentage of deposits currently loaned to borrowers. The table shows that interest rates and utilization rates can vary significantly between stablecoins, which largely do not fluctuate in value, and well-established but still volatile crypto assets.

The Top Five Lending Markets in DeFi Consist of Stablecoins and the Most Established Crypto Assets

Aave and Compound’s top five lending markets as of May 4, 2022 (USD billion)

This table provides a view into how DeFi protocols have learned to balance incentives for lenders and borrowers to promote capital efficiency, while also maintaining the solvency of their lending pools—across very different types of assets. What we see, broadly, over the last two years is less the creation of new tools than the continuous refinement of existing tools, based on learnings from millions of transactions and tens of thousands of users.

In the present configuration that the leading DeFi protocols use, several asset-specific risk parameters control each lending pool, including most importantly: collateral factors, interest rate models, and reserve factors. DeFi lending protocols attempt to optimize those parameters to balance risk and reward through a dynamic risk management and governance process in which Aave and Compound token holders can participate.

Collateral factors limit the amount users can borrow against their deposited collateral. If the value of the collateral securing a loan falls below the required collateral factor, liquidators can purchase the collateral at a discount (like foreclosure sales in traditional markets).

Setting appropriate collateral requirements is a critical element of ensuring protocol solvency. Assets with deeper liquidity and less volatility tend to have higher collateral factors. Conversely, more volatile assets with less liquidity generally have lower collateral factors. However, too low collateral factors can inhibit existing borrowers and deter new ones, reducing borrowing power for users but helping ensure solvency in times of high volatility. At the same time, higher collateral factors can unlock borrowing power for existing and new users.

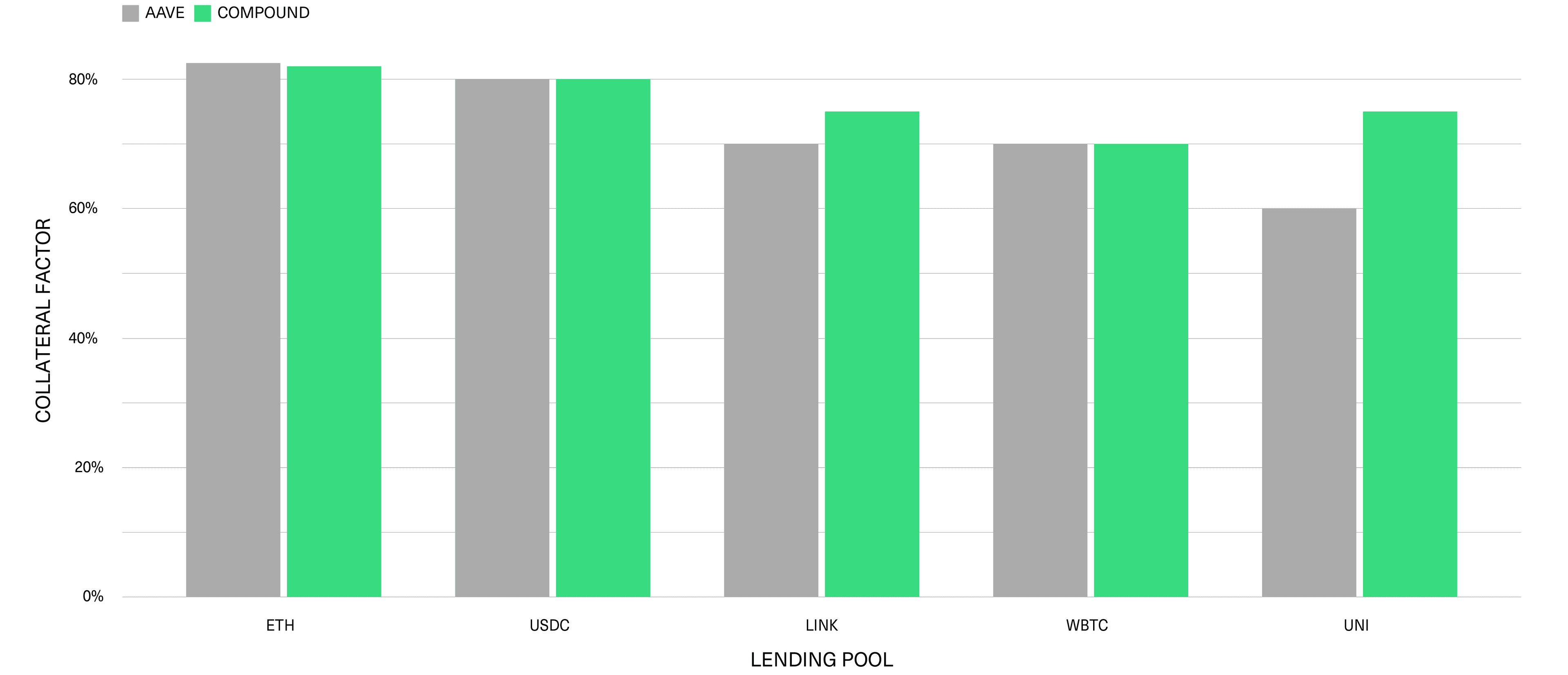

The chart below shows the collateral factors for each of the top five pools in Compound and Aave. Part of the ongoing risk management of the protocol requires assessing and adjusting the collateral factors for all assets.

More Volatile Assets With Less Liquidity Have Lower Collateral Factors

Compound and Aave’s collateral factors for select markets as of May 4, 2022

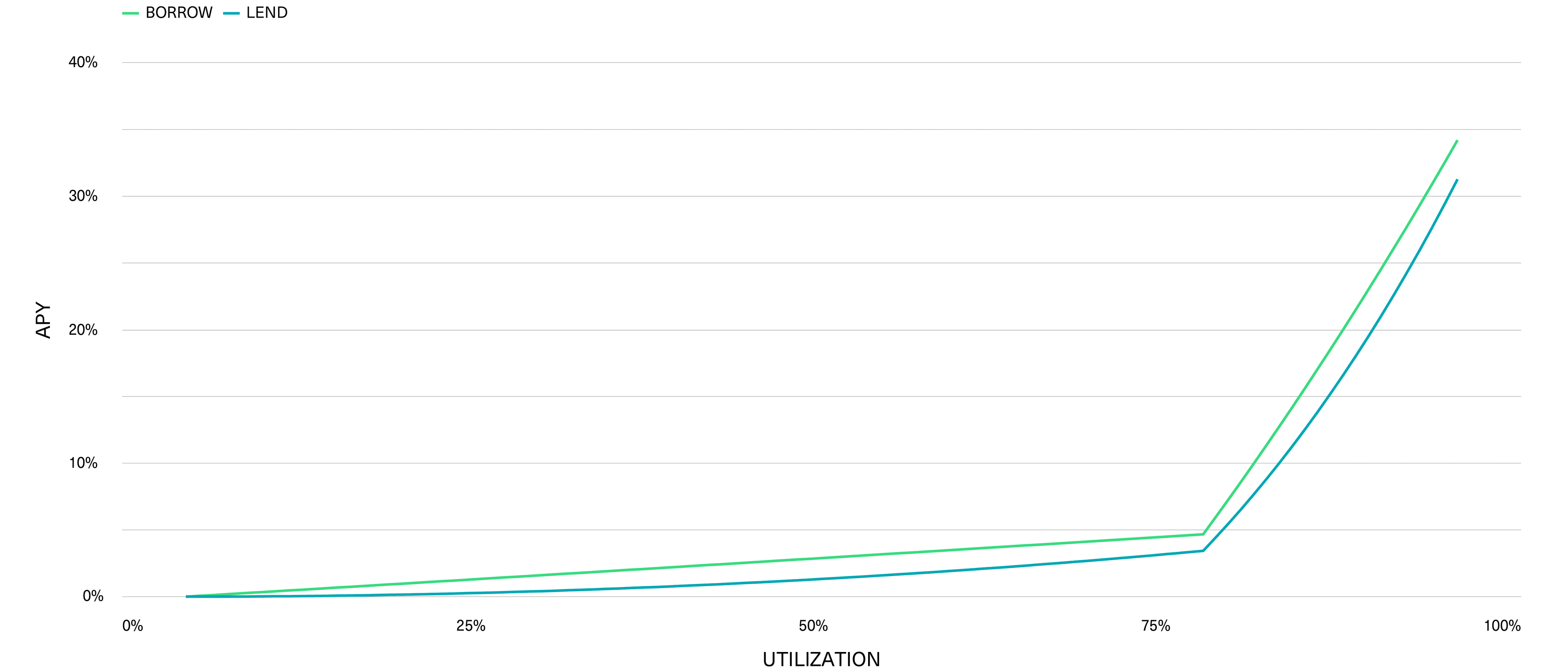

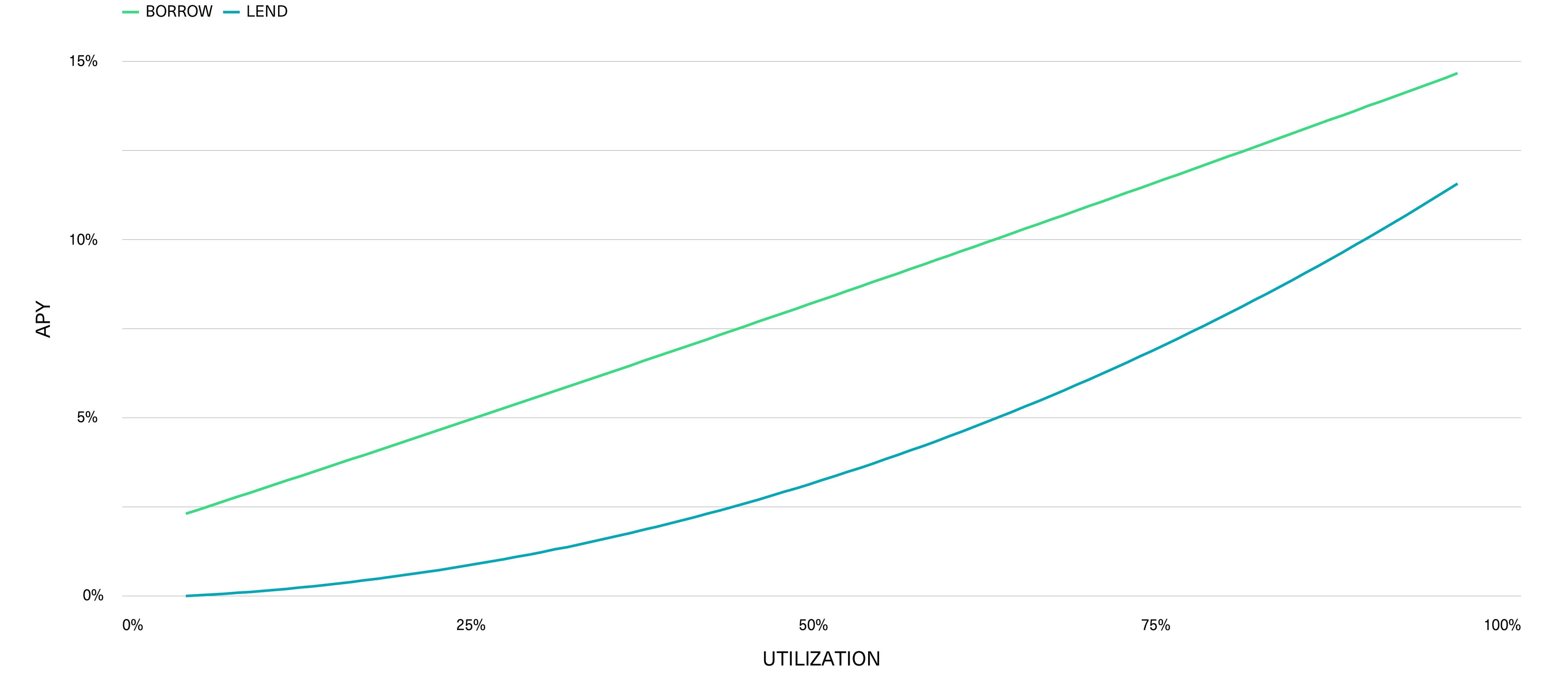

Interest rate models define the rate for lending or borrowing a given asset based on the supply of capital and demand for borrowing. They use bonding curves, which determine the rates depending on the lending pool's utilization at a given moment—as a pool’s utilization increases (i.e. demand increases), so does the interest rates to lend and borrow assets to and from that pool (i.e. interest rates increase). The charts below show the interest rate models that Compound actively uses for USDC and ETH, two of the largest and most widely used assets in DeFi credit markets.

Stable Assets Like USDC Support Higher Utilization

The Compound platform’s interest rate model for USDC

Volatile Assets Like ETH Are Modeled for Lower Utilization

The Compound platform’s interest rate model for ETH

The differently shaped curves result from the specific risk profiles of ETH and USDC. For example, a flatter curve that supports higher utilization rates is well suited for stablecoins (with low volatility). Conversely, a steeper curve that forces a more dramatic increase in interest rates at lower utilization rates reflects the risk-averse strategy commonly used with more volatile, non-stable crypto assets like ETH.

Monitoring and optimizing the interest rate models for each lending pool is perhaps the most critical risk management tool, with the goal being to adequately balance the risk of insolvency with the rewards of higher utilization. This tradeoff significantly impacts user and revenue growth.

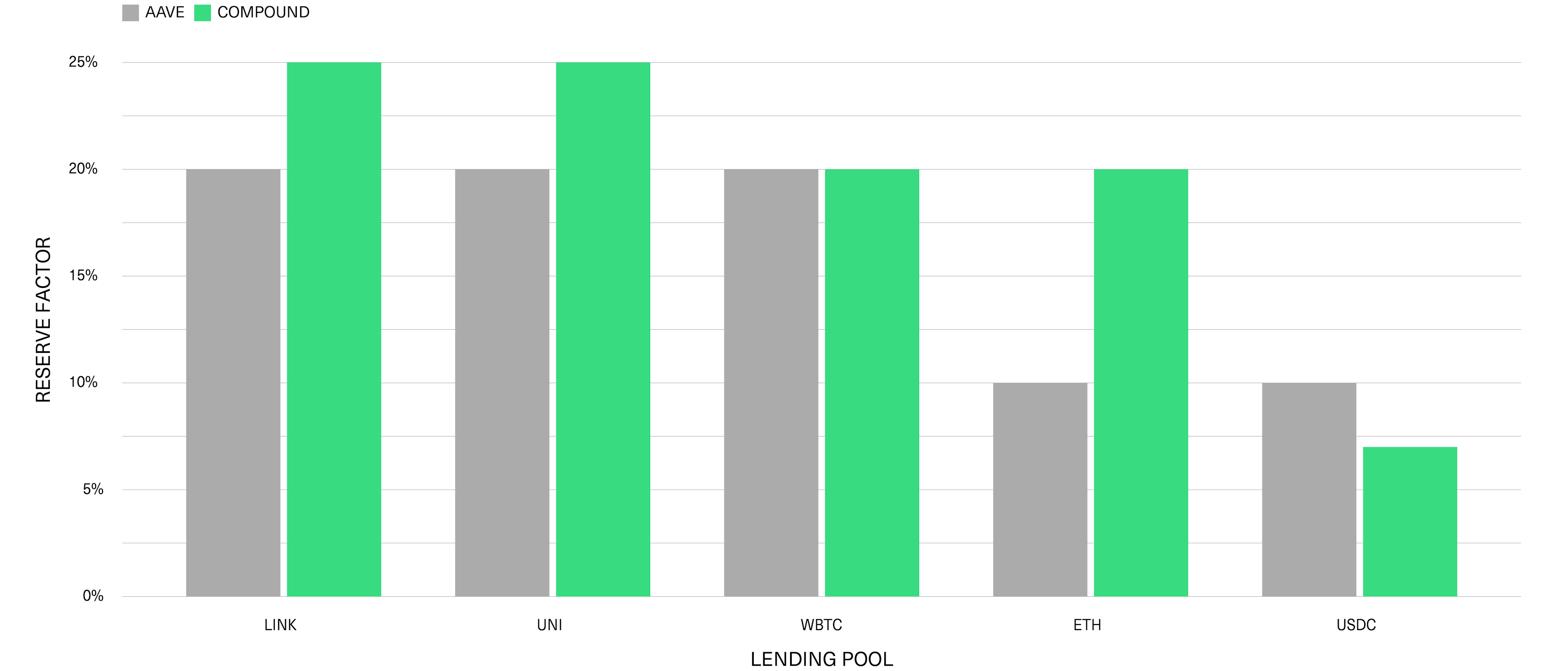

Protocol reserves exist in case of emergencies resulting in funds loss, such as liquidation failures and smart contract failures. A lending pool's reserve factor defines the amount of interest revenue allocated to protocol reserves.

For Compound, the reserves are like a provision for bad debt: A portion of the spread between borrowers and lenders is set aside for a rainy day. For Aave, the reserves are used to fund growth of the Aave ecosystem through user incentives and grants, while their "rainy day" fund comes from users who stake their Aave token and the protocol's safety module.

For both protocols, the reserve factor increases as assets move along the volatility spectrum, from stablecoins to more volatile crypto assets. In this way activity in more volatile assets contributes to the overall stability of the protocol.

Reserve Factors Redirect a Portion of Interest Revenue to the Protocol Reserves

Compound and Aave’s reserve factors for select markets as of May 4, 2022

The aim, as with the other risk parameters, is to strike a balance between protocol safety, user experience, and incentives. For example, lowering the reserve factor can increase yields for lenders or lower the interest rate for borrowers. However, that could reduce assets flowing into the reserves, reducing the size of the protocol's backstop and growth budget.

At the same time, protocols must balance the possibility that increasing the reserve factor may be a better long-term growth strategy. For example, more extensive reserves allow for riskier loans across a broader universe of assets, including those further along the risk curve or even un-collateralized lending, which may increase the protocol’s activity and user base.

The Evolution of Risk Management in DeFi

Over the last couple of years, risk management has significantly improved in DeFi credit markets as protocols have fine-tuned and differentiated critical risk parameters across a growing number of lending pools.

One positive outcome from this is the increase in capital efficiency and borrower activity that’s led to more revenue for lenders and token holders. For example, since the beginning of 2020 (before the March crash), the lending sector has grown to more than $49 billion in total deposits. That’s partly due to lending protocols expanding the universe of assets they support and the corresponding impact on lender and borrower activity. And yet, despite multiple price corrections of over 30% in the crypto market, these protocols have weathered the storm. Their ability to scale while systematically balancing capital efficiency with protocol resiliency is one of the pillars that supports our long-term confidence in the leading DeFi borrowing and lending protocols.

Another is the speed at which protocols are now able to onboard new assets and accelerate growth. For example, Aave recently introduced isolated lending pools (similar to Rari Capital’s Fuse application) that reduce the risk associated with onboarding newer assets by placing supply caps and other limitations on the lending pools, such as types of assets that users can borrow against them. As these types of assets mature, become more stable, and gain more liquidity, the initial limitations can be adjusted, ultimately allowing for asset scalability. These are essential improvements that support further growth of lending and borrowing platforms, particularly as they expand into markets that are less liquid or carry more risk.

Importantly, all these risk parameters are monitored and managed through a dynamic governance process in which every token holder has a voice. This transparent and open risk management system is an overlooked factor by which DeFi improves upon the legacy financial system.

That’s why specialized companies focusing on risk management and protocol optimization are already attaining unicorn status. Gauntlet, for example, creates and manages simulation models based on user and market data that inform the risk management process for Aave, Compound, and other DeFi protocols. They run simulations under various market conditions and generate the optimal protocol parameter designs to optimize risk and reward. Those proposed parameters are voted on by token holders and (if approved) implemented by protocol developers. Post-implementation, Gauntlet's models continue to monitor how the changes impact the actual performance of the protocol, and the findings help fine-tune the models for the next cycle of risk management updates. This is dynamic risk management in action.

What if everyone could inspect the credit book of a financial institution, and its shareholders could vote on proposed changes to optimize the business in real-time? It's already happening in DeFi. It’s another factor that makes us excited about the fundamentals of this industry, and it’s another way in which it can substantially improve upon the legacy financial system.

(1) Emilio Frangella, “Crypto Black Thursday: The Good, the Bad, and the Ugly,” Medium, March 19, 2020, https://medium.com/aave/crypto-black-thursday-the-good-the-bad-and-the-ugly-7f2acebf2b83https://medium.com/aave/crypto-black-thursday-the-good-the-bad-and-the-ugly-7f2acebf2b83.

(2) Watson Fu, “Aave Protocol Liquidation Retrospective: May 2021,” Medium, June 4, 2021, https://medium.com/gauntlet-networks/aave-protocol-liquidation-retrospective-may-2021-67c655fc1b31https://medium.com/gauntlet-networks/aave-protocol-liquidation-retrospective-may-2021-67c655fc1b31.

(3) Gauntlet’s “Market Downturn Report: Gauntlet Risk Review (Jan 2022)” for Compoundhttps://www.comp.xyz/t/market-downturn-gauntlet-risk-review-jan-2022/2911 and Aavehttps://governance.aave.com/t/market-downturn-gauntlet-risk-review-jan-2022/7190.

Disclosure: This material represents the views of the author and does not represent the views of Bitwise Asset Management.

About Bitwise

Bitwise Asset Management is the largest crypto index fund manager in America. Thousands of financial advisors, family offices, and institutional investors partner with Bitwise to understand and access the opportunities in crypto. For six years, Bitwise has established a track record of excellence managing a broad suite of index and active solutions across ETFs, separately managed accounts, private funds, and hedge fund strategies. Bitwise is known for providing unparalleled client support through expert research and commentary, its nationwide client team of crypto specialists, and its deep access to the crypto ecosystem. The Bitwise team of more than 60 professionals combines expertise in technology and asset management with backgrounds including BlackRock, Millennium, ETF.com, Meta, Google, and the U.S. Attorney’s Office. Bitwise is backed by leading institutional investors and has been profiled in Institutional Investor, Barron’s, Bloomberg, and The Wall Street Journal. It has offices in San Francisco and New York. For more information, visit www.bitwiseinvestments.com.