Stablecoins: Separating the Wheat From the Chaff

San Francisco • Jun 28, 2022

Stablecoins are often referred to as “the killer application for crypto.” While they first emerged as a reliable way to trade in and out of more volatile assets like bitcoin, as their use cases have grown they have become one of the most heavily used assets across the crypto economy.

Not all stablecoins are created equal, however. There are different ways to design a stablecoin, and each approach carries its own technical, implementation, and regulatory risks. The recent high-profile collapse of the TerraUSD stablecoin has made it very clear that investors, regulators, and users need to understand these different designs and their varying trade-offs.

Like separating the wheat from the chaff, separating the good stablecoin designs from the bad is a necessary step in their development. Below, we explore the purpose of stablecoins, their different types, what design structures have and haven't worked, and why regulators—particularly in the U.S.—should be embracing them.

So, Why Do Stablecoins Exist?

A stablecoin is a crypto asset that is pegged to the value of a real-world asset. For example, one USD Coin is always intended to be worth one U.S. dollar. What makes them useful is that they hold their value relative to traditional currencies but, unlike the money in your bank account, stablecoins can be traded freely on the blockchain.

Stablecoins serve many of the same purposes in crypto markets as the U.S. dollar in traditional markets. They’re used for everything from saving and trading to sending and lending, and they’ve been adopted by a range of users, from crypto enthusiasts to traditional financial institutions.

For instance, an investor who holds bitcoin or another crypto asset may want to sell that position but not withdraw money into the slow-moving traditional financial system; instead, they trade into a stablecoin. Likewise, in a country facing high inflation, like Argentina, people may prefer to park their assets in a stablecoin, which can be an easier way of gaining access to the dollar and broader financial services than accessing U.S. banks.

For people getting paid for work done abroad or sending money to family back home, the low-cost, high-speed features of stablecoins can have a meaningful impact. When combined with DeFi lending protocols like Aave and Compound, stablecoins can provide access to financial services and change the financial reality of millions of people worldwide.¹

In sum, stablecoins offer a more cost- and time-efficient way of exchanging value than the decades-old payment rails that the global financial system relies on today. They are transferable 24/7/365 (blockchains don’t observe banking hours or holidays) and are faster and cheaper to transact with than their fiat counterparts (blockchain transactions typically settle within seconds, and the fees are a function of the underlying network’s usage instead of a percentage of the transaction value).

That’s why stablecoins have continued to rise in popularity through bull and bear markets.

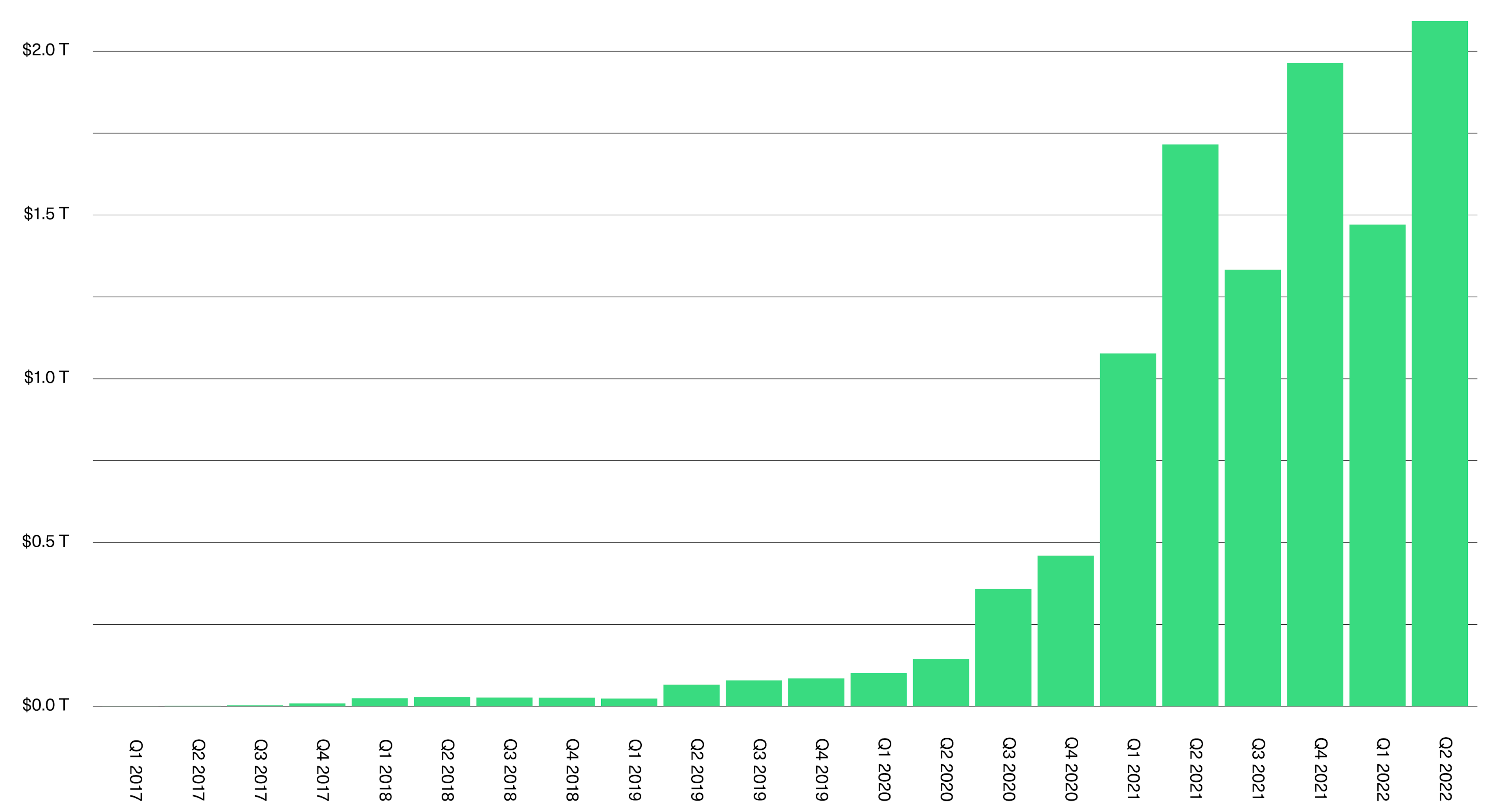

The Value Settled Using Stablecoins Is on Track for a Record Quarter

Value of stablecoin transfers between January 2017 and June 2022* (USD trillions)

Next Question: Why Are There Different Types of Stablecoins?

Most stablecoins are crypto assets whose value is pegged to another currency like the U.S. dollar. The three prevailing models for stablecoin are fiat-collateralized, crypto-collateralized, and algorithmic. Under the hood, each type works differently and, crucially, has different pros and cons.

Fiat-collateralized stablecoins function much like traditional money market funds. An investor deposits $1 with a centralized issuer, which in exchange issues a stablecoin representing that dollar. (This process is referred to as “minting” a stablecoin.) The issuer then invests that dollar in yielding assets—typically Treasuries and short-term commercial paper. The investor gets the liquid stablecoin to use in the crypto market, and the issuer earns interest on the deposit.

The key promise is that you can always redeem the stablecoin for $1 from the issuer. (Typically the issuer will then remove from circulation, or “burn,” the stablecoin that is redeemed.)

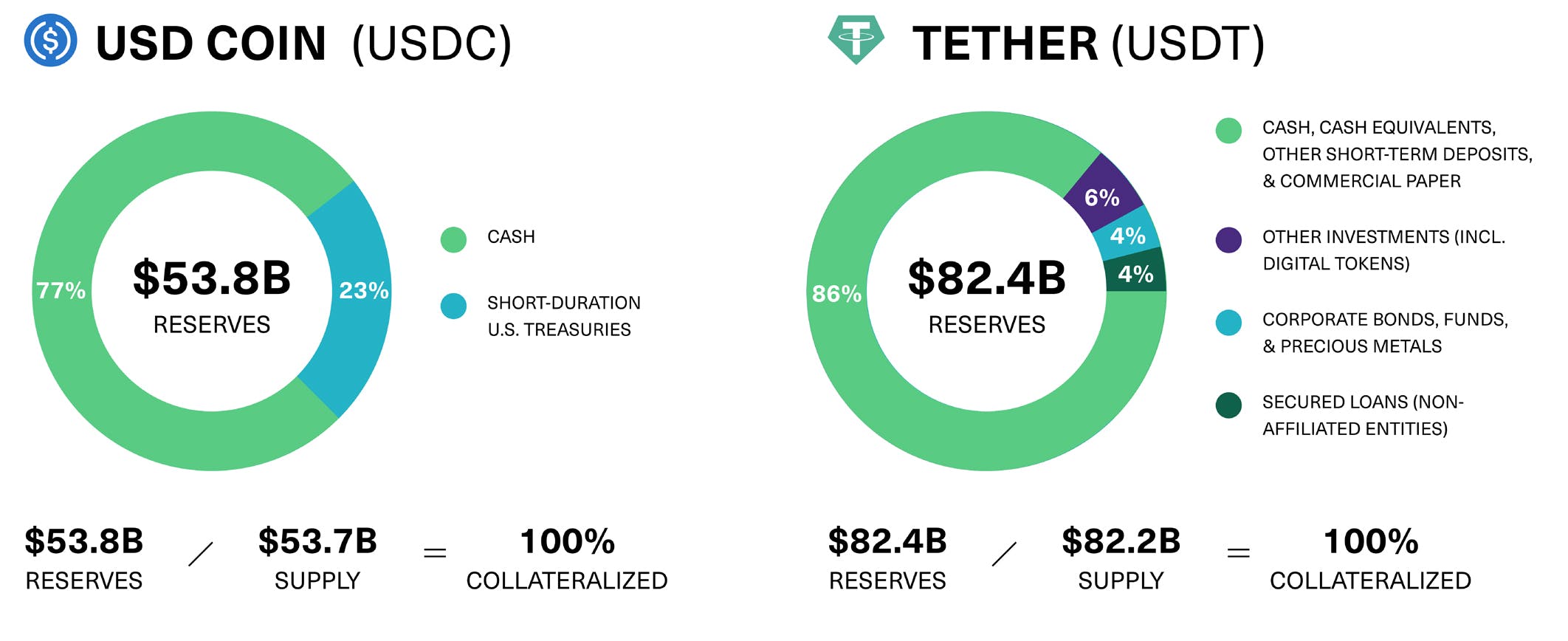

Fiat-collateralized stablecoins are the most popular and widely used, led by USD Coin (USDC) and Tether (USDT). The downside is that centralized issuers lack transparency. Investors have to trust that the issuer actually has sufficient reserves in their bank account and that investors can redeem as needed. And when you look more closely, the reserves held by different issuers present very different risk profiles.

Reserves Held by the Issuers of the Leading Fiat-Collateralized Stablecoins

For market participants searching for relatively lower risk within the stablecoin space, Tether’s 10% allocation to digital tokens and precious metals might cause concern around its liquidity in the event of a market crash or bank run. In contrast, as the charts above show, USDC is allocated solely to Treasuries and cash.

Perhaps that helps explain why USDT’s dominance in the stablecoin market has fallen from 81% to 50% since 2020.

Crypto-collateralized stablecoins are the second-most popular type of stablecoin. They operate more like traditional home equity loans: An investor deposits crypto assets with a decentralized issuer (usually a DeFi protocol), which issues stablecoins in exchange. The investor gets to use their stablecoins however they’d like but must repay the stablecoins—plus a fee—to redeem their crypto assets. Suppose the value of the crypto assets falls too far; in that case, the investor can repay the stablecoins or deposit more collateral. Otherwise, the DeFi protocol will automatically sell the crypto being used for collateral and repay the stablecoins for them. Of course, this carries more fees.

With this design, the critical promise is that every stablecoin in circulation is directly backed by excess collateral. Furthermore, from a transparency perspective, since crypto assets reside “on chain,” the reserves can be audited and monitored by anyone in real time (including regulators).

Unfortunately, over-collateralization leads to lower capital efficiency, and that’s not ideal. But on the other hand, it helps hedge the volatility risk associated with the crypto assets that make up their reserves. Using crypto assets rather than fiat currency can also offer fewer ties to the traditional financial system, which some investors see as a way to limit systemic risk.

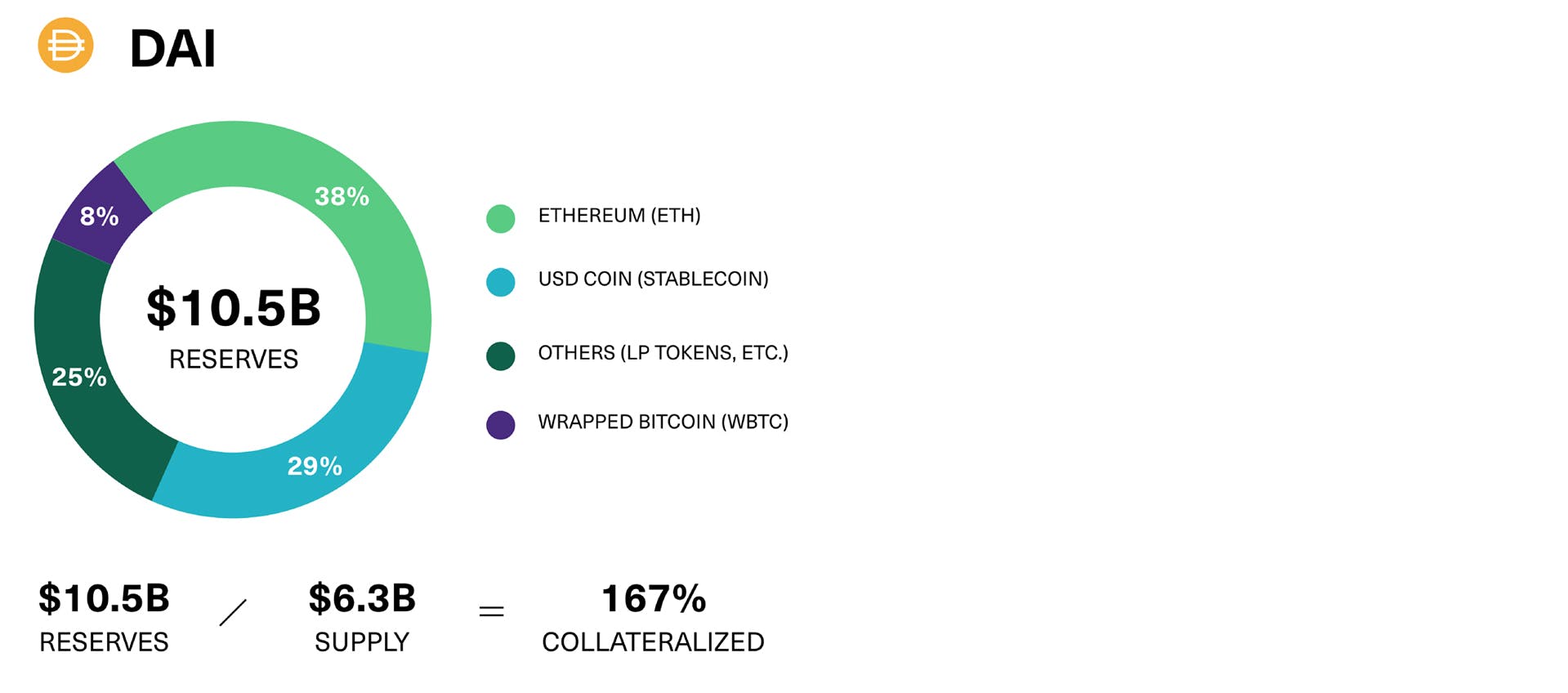

Let’s look at DAI, the leading crypto-backed, over-collateralized stablecoin. The 6.3 billion DAI in circulation is backed by more than $10 billion of crypto reserves, giving it a collateralization ratio of 167%.

Reserves Held by the Leading Crypto-Backed, Over-Collateralized Stablecoin

Then there are algorithmic stablecoins, which function similarly to central banks. (If you’ve ever heard of Terra or its stablecoin TerraUSD, you can probably guess where this is headed.)

Algorithmic stablecoins are typically minted and issued by a DeFi protocol. They are commonly under-collateralized, meaning they are not backed by an equivalent or excess amount of collateral. In other words, just because an algorithmic stablecoin is pegged to the value of a real-world asset or fiat currency, that doesn’t mean it’s backed by one.

Instead, they mostly rely on an algorithm that aims to maintain a stable price by expanding and contracting the supply of the stablecoin. The intent is to influence interest rates and market behavior, which, in theory, ultimately return the stablecoin to its target price. It’s similar to how the Federal Reserve uses monetary policy to influence market behavior, e.g., by raising and lowering interest rates.

The key promise is that the algorithm and incentive mechanisms work as promised, and the stablecoin maintains its peg through the issuance and removal of its circulating supply.

The most apparent downside is that the algorithmically structured, non-collateralized model continues to fail. As a result, even some algorithmic stablecoins have embraced a hybrid model (i.e., partially backed by crypto assets). The most popular such hybrid was TerraUSD before it famously ended in a $19 billion death spiral. The failed stability algorithm and a massive collateral deficit led to the price of TerraUSD falling from $1.00 to $0.10 over the course of a few days.

The failure of TerraUSD was an event that shook the foundations of crypto. One consequence has been that the market for algorithmic and under-collateralized stablecoins has quickly dried up—they now represent less than 3% of the stablecoin market, down from 14% before TerraUSD collapsed.

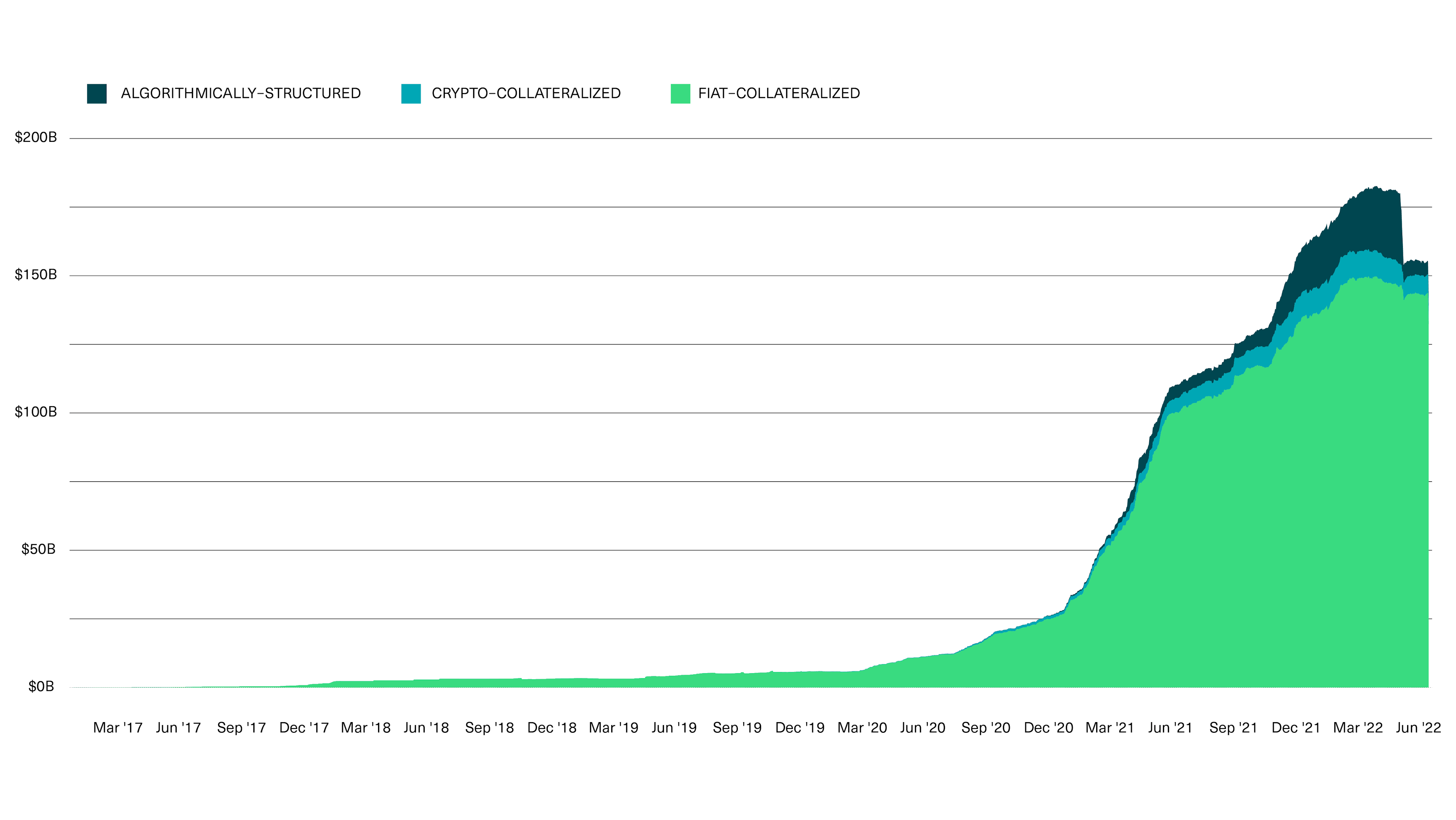

Fiat-Backed Stablecoins Represent 93% of the Total Stablecoin Supply

Total stablecoin supply by type from January 1, 2017, to June 20, 2022 (USD billions)

Crypto- and fiat-backed stablecoins have a much better track record than their algorithmic counterparts. As the above chart illustrates, fiat-backed stablecoins, in particular, are the clear market leader for now. That makes sense—they have the simplest design, are fully collateralized, and have been around for years.

Finally: Why Should Regulators Embrace Stablecoins?

It's relatively simple: Most stablecoins in circulation today are backed by and denominated in the U.S. dollar (and cash equivalents like U.S. Treasuries). To put it plainly, the dominant use of USD-backed stablecoins across the crypto economy promises to extend the U.S. dollar's dominance into the Metaverse.

In that light, it's surprising how long it has taken for most U.S. regulators to understand that stablecoins are bullish for the U.S. and dollar supremacy.

Nonetheless, some politicians and regulators are starting to recognize the improvements that stablecoins can offer to global payment rails, infrastructure, and financial access. Last November, the U.S. Treasury’s Report on Stablecoins noted, "If well-designed and appropriately regulated, stablecoins could support faster, more efficient, and more inclusive payments options." Maybe they're starting to understand that stablecoins don't threaten dollar supremacy—they amplify it.

Regulators and blockchain technology will inevitably converge, and a prime location for this rendezvous is stablecoins. Within the crypto community, it's essential to distinguish between the viable stablecoin projects (like fiat-backed and over-collateralized, crypto-backed stablecoins) and the unproven (like under- or non-collateralized algorithmic stablecoins).

Only then can we hope to realize the promise that stablecoins—and crypto—offer to the world. Imagine a low-cost, secure, universally accessible way of instantly moving "dollars'' around the world. That's what stablecoins can offer—the properly designed ones, at least.

(1) Mariano Conti, “Living on Defi: How I Survive Argentina's 50% Inflation,” Ethereum Devcon5, October 9, 2019, https://slideslive.com/38920018/living-on-defi-how-i-survive-argentinas-50-inflation.

Important Disclosures

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not currently backed nor supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional currencies, stocks, or bonds.

Trading in cryptocurrencies comes with significant risks, including volatile market price swings or flash crashes, market manipulation, and cybersecurity risks and risk of losing principal or all of your investment. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing.

Cryptocurrency trading requires knowledge of cryptocurrency markets. In attempting to profit through cryptocurrency trading, you must compete with traders worldwide. You should have appropriate knowledge and experience before engaging in substantial cryptocurrency trading. Cryptocurrency trading can lead to large and immediate financial losses. Under certain market conditions, you may find it difficult or impossible to liquidate a position quickly at a reasonable price.

Bitwise Asset Management is a global crypto asset manager with $9 billion in client assets and a suite of over 70 investment products spanning ETFs, separately managed accounts, private funds, hedge fund strategies, and staking. The firm has a nine-year track record and today serves more than 5,500 private wealth teams, RIAs, family offices and institutional investors as well as 21 banks and broker-dealers. The Bitwise team of technology and investment professionals is backed by leading institutional investors and has offices in San Francisco, New York, and London.